used car financing, used car loans, vehicle age limits, auto loan interest rates, loan terms for older cars, credit unions auto loans, personal loan for car

Published Date:

Feb 25, 2026

Last Updated:

Feb 25, 2026

How Age Impacts Used Car Financing Options

When financing a used car, the vehicle's age is a major factor in determining your loan options, interest rates, and approval chances. Lenders view older cars as riskier due to depreciation, lower resale value, and higher repair costs. Here’s what you need to know:

Lender Restrictions: Most banks won’t finance cars older than 10 years or with mileage over 120,000. Some, like PNC Bank, have stricter limits (9 years, 100,000 miles). Credit unions or platforms like Upstart may allow financing for cars up to 13 years old.

Higher Interest Rates: Older cars come with steeper rates - averaging 13.8% for vehicles 9+ years old, compared to 10.2% for cars under 3 years.

Shorter Loan Terms: Loans for older cars often max out at 36-60 months, leading to higher monthly payments.

Alternative Options: If traditional loans are unavailable, consider credit unions, personal loans, or increasing your down payment to reduce lender risk.

Key Tip: Compare lenders, check your credit score, and explore flexible options like credit unions to secure better terms when financing older vehicles.

Lender Restrictions on Older Vehicles

Age and Mileage Limits

When it comes to financing used cars, most lenders stick to a strict rule: they won't finance vehicles older than 10 model years. This policy helps protect lenders from the rapid depreciation that older cars typically experience. As Dave Goldberg, a former car salesman, puts it:

"The banks we worked with had a hard cutoff of 10 model years for financing (and mileage restrictions also came into play, with the cutoff being around 100,000-120,000 miles)" [3].

While this is standard practice, some lenders offer slightly more lenient terms. For example, Upstart might finance cars up to 13 years old with mileage up to 140,000, whereas PNC Bank is more conservative, capping their limits at 9 years and 100,000 miles [2].

Why do these limits exist? High mileage often means more wear and tear, which leads to higher repair costs and faster depreciation. For lenders, this increases the risk that if they need to repossess the car, its value won’t cover the remaining loan balance [2] [3]. These concerns also influence how lenders evaluate borrowers, as we'll see in the next section.

How Restrictions Affect Loan Approval

These age and mileage limits directly impact loan approval processes. If a vehicle doesn't meet a lender's criteria, your application may be rejected outright. This leaves many buyers looking at alternative options, such as unsecured personal loans. However, these loans often come with higher interest rates - averaging around 11.48%, compared to the roughly 7.48% typical for auto loans [5].

Even if your vehicle qualifies, lenders might still require a larger down payment. This is tied to the Loan-to-Value (LTV) ratio, which measures how much a lender is willing to finance relative to the car's current market value. When the LTV ratio is high, lenders often demand down payments of 10–20% or more to reduce their risk [2] [3].

For buyers on a tight budget, these restrictions can make financing older, more affordable vehicles particularly challenging. Not only do these rules affect whether you get approved, but they also play a role in determining your interest rate, making it harder to secure favorable terms for older cars.

How to Finance a car older than 10 years! + Giveaway update

Interest Rates and Financing Costs for Older Cars

Used Car Financing Costs by Vehicle Age: Interest Rates and Payment Comparison

Higher Interest Rates for Older Vehicles

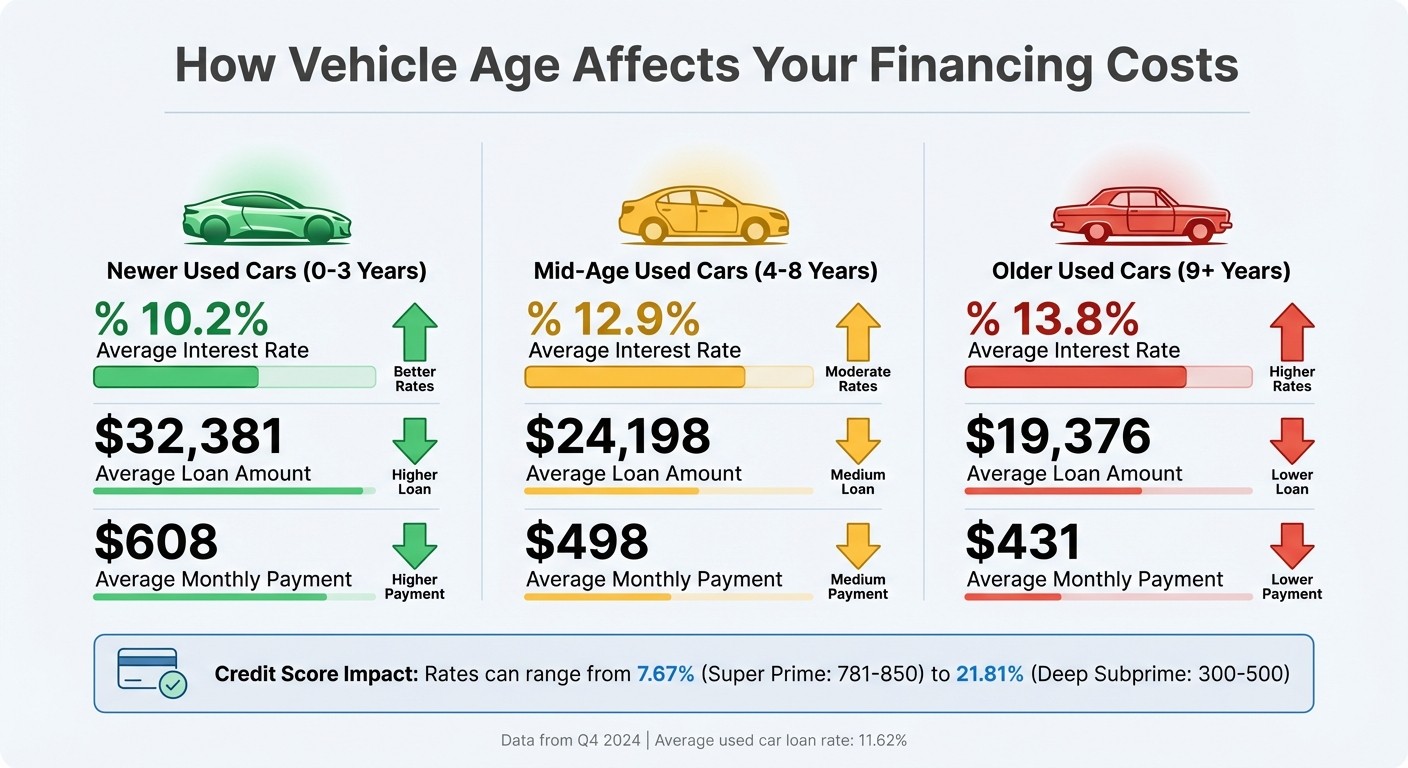

When it comes to financing older cars, the numbers don’t lie: the older the car, the higher the interest rate. In Q4 2024, the average interest rate for used car loans reached 11.62%, almost double the 6.35% average for new car loans [8]. Breaking it down further, vehicles aged 0-3 years had an average rate of 10.2%, while cars 9 years or older climbed to a hefty 13.8% [6].

So why do older cars come with steeper rates? Meghan Carbary, Automotive Content Editor at CarsDirect, sheds light on this:

"Used vehicles typically cost more to finance than new cars... because older vehicles are financed by borrowers with lower credit scores, have lower resale values, have more mechanical issues, [and] have higher repossession rates" [4].

In short, lenders see older vehicles as a greater risk.

Credit Scores and Risk Factors

When financing a car, your credit score plays a huge role - sometimes even more than the car's age. Lenders assess both your creditworthiness and the vehicle’s age to determine your rate. For example, in Q4 2024, borrowers with "Super Prime" credit scores (781-850) averaged a 7.67% APR on used cars. Meanwhile, those in the "Deep Subprime" category (300-500) faced rates as high as 21.81% [8]. That’s nearly triple the rate for top-tier borrowers.

Financing an older car with a low credit score creates what lenders call a "double risk." Both the borrower and the vehicle are seen as higher risk, leading to some of the steepest interest rates. If you’re in this situation, working to improve your credit score before applying for a loan can make a noticeable difference [2][8].

Financing Terms by Vehicle Age

The impact of these risk-based interest rates extends to loan terms, as shown below:

Vehicle Age | Avg. Interest Rate | Avg. Loan Amount | Avg. Monthly Payment |

|---|---|---|---|

0-3 Years | 10.2% [6] | $32,381 [6] | $608 [6] |

4-8 Years | 12.9% [6] | $24,198 [6] | $498 [6] |

9+ Years | 13.8% [6] | $19,376 [6] | $431 [6] |

While older vehicles come with higher interest rates, they often involve smaller loan amounts, which can help keep monthly payments manageable. In fact, in 2024, prime and super prime borrowers financed nearly 54% of vehicles aged 9 years or older, a jump from 42.5% just five years earlier [6]. This trend shows that higher-credit buyers are increasingly turning to older cars to keep their monthly payments below $450.

Loan Terms for Older Vehicles

Shorter Loan Terms for Older Cars

When financing an older vehicle, expect a shorter repayment period. While the average used car loan term reached 67.2 months in Q4 2024 [7], loans for older cars usually fall between 36 and 60 months. This is largely because lenders aim to minimize risks tied to depreciation and potential repair costs.

Finance expert Ben Luthi from Experian highlights this point:

"Older vehicles with high mileage pose more of a risk of breaking down, so you can generally expect shorter repayment term options." [7]

Lenders like PenFed Credit Union reflect this approach in their policies. For example, they only offer 84-month terms for cars under five years old with fewer than 60,000 miles [2]. For vehicles that exceed age or mileage limits - like those with over 150,000 miles - loan terms may be capped at 36 months or less [9]. If you're considering a car that's close to or over 10 years old, credit unions often provide more flexible options compared to national banks [4].

Monthly Payment Differences

Shorter loan terms mean higher monthly payments. Even though older cars are less expensive to finance, the compressed repayment period results in larger principal payments each month. As The Auto Lot explains:

"Buyers should be prepared for higher monthly payments relative to the amount borrowed, as lenders seek to mitigate risk through a more aggressive repayment schedule." [1]

The upside? You'll pay less interest over the life of the loan and build equity faster, reducing the chances of owing more than the car's value. This is one reason why nearly 30% of used car buyers now choose loan terms of 60 months or less [7]. Shorter terms help avoid the negative equity trap that can arise from stretching payments out too long. However, if these higher payments feel unmanageable, a personal loan might be worth exploring, even though it typically carries higher interest rates [3].

Strategies for Financing Older Vehicles

Financing an older vehicle comes with its own set of challenges, but with the right approach, you can navigate these hurdles effectively. Exploring a variety of lender options and tailoring your strategy can make all the difference.

Compare Multiple Lenders

Taking the time to compare lenders can save you thousands - on average, borrowers save $5,198 by shopping around [11]. Different lenders have varying rules for vehicle age and mileage. For example, credit unions tend to be more accommodating, often financing vehicles up to 15 years old [2]. Getting pre-qualified with multiple lenders before heading to a dealership not only clarifies your budget but also strengthens your position during negotiations [10]. Once you’ve done this, you can look into dealerships that cater specifically to older vehicles.

Dealership Financing Options

Used car dealerships often have access to indirect financing through subprime lenders who are more open to working with older vehicles [4]. For instance, Hello Motors, a dealership based in Ontario, provides financing options for buyers across all credit profiles and vehicle ages. Their process includes online applications for quick approvals and personalized assistance throughout the financing journey. This can be a great route for buyers who may have been turned down by banks or credit unions due to the vehicle's age or their credit history.

Alternative Financing Methods

If traditional loans are hard to secure, there are other ways to finance an older car. Increasing your down payment is a smart move - it lowers the loan-to-value ratio, reducing the lender’s risk and boosting your chances of approval [2][10]. Another option is a personal loan, though these often come with higher interest rates. For instance, as of July 2023, the average interest rate for a two-year personal loan was 11.48%, compared to 7.48% for a 60-month new-car loan [5]. If you have access to a co-signer with strong credit, you might qualify for better rates and terms [2]. Keep in mind that most lenders will require full coverage insurance for the loan’s entire duration, no matter how old the vehicle is [2][10].

Conclusion

The age of a vehicle plays a major role in determining financing options, shaping everything from interest rates to loan eligibility. As Dave Goldberg from Jalopnik puts it, "Age and condition matter because the bank wants to know it can recover its money if you default on the loan" [3]. Essentially, the car acts as collateral, and its age and mileage set the boundaries for financing terms.

To navigate these boundaries effectively, start by checking your credit score - most traditional banks look for a score of 670 or higher for used vehicle loans [4]. If your car falls outside standard lending criteria, options like credit unions, specialized lenders, or even unsecured personal loans might still be available. However, these alternatives often come with higher interest rates, so balancing them against your budget is essential.

While the lower price tag of an older car might seem appealing, don’t overlook the bigger picture. Higher interest rates and potential repair expenses can sometimes make an older vehicle costlier in the long run compared to a slightly newer model [1][4]. Additionally, lenders usually won’t finance amounts that exceed the car’s appraised value, so ensure the purchase price aligns with its book value [4].

Shopping around for financing is crucial, especially when dealing with age-related restrictions. Getting pre-qualified can give you a stronger negotiating position without affecting your credit score [2][12]. Whether you’re working with a bank, credit union, or a dealership like Hello Motors that caters to all credit types, understanding how vehicle age impacts financing gives you the upper hand.

With the average car on U.S. roads now nearly 13 years old [3], lenders are adjusting to the reality of longer-lasting vehicles. By improving your credit score, increasing your down payment, and comparing offers, you can overcome challenges tied to vehicle age and secure terms that work for your financial situation.