How co-signing a car loan in Ontario works: legal liability, credit impact, risks, and practical steps to protect your finances before you sign.

Published Date:

Jan 17, 2026

Last Updated:

Jan 17, 2026

How Co-Signing Works for Ontario Car Loans

When you co-sign a car loan in Ontario, you agree to take full responsibility for the loan if the borrower doesn't pay. Co-signers don't own the vehicle, but their credit and financial stability are critical to the loan's approval. Here's what you need to know:

Why Co-Signing Happens: Borrowers with poor credit, no credit history, or unstable income may need a co-signer to qualify for a loan.

Legal and Financial Responsibility: Co-signers are fully liable for the loan, including missed payments, late fees, and any balance owed after repossession.

Impact on Credit: The loan appears on the co-signer's credit report, affecting their debt-to-income ratio and ability to secure future loans. Late payments can significantly lower their credit score.

Risks: If the borrower defaults, the co-signer must repay the entire loan. Co-signers don't have ownership rights to the vehicle.

How to Protect Yourself: Monitor payments, ensure the borrower can afford the loan, and review all terms before signing.

Co-signing helps borrowers access financing but comes with serious risks. If you're ready to browse inventory and explore your options, ensure you're financially prepared before agreeing to co-sign. Make sure you're financially prepared before agreeing to co-sign.

What Banks DONT Tell You About Co-Signing Car Loans

What Is a Co-Signer for Car Loans in Ontario?

A co-signer is someone who guarantees a car loan’s repayment but doesn’t have ownership of the vehicle. Essentially, they’re vouching for the borrower’s ability to pay back the loan, which reassures lenders - especially when the borrower has poor credit or limited income. It’s important to note that while the co-signer doesn’t own the car, they are equally responsible for repaying the loan in full. This arrangement depends heavily on the co-signer’s strong financial standing, which lenders evaluate carefully.

"If the borrower defaults on the loan, the co-signer is legally responsible for repaying the loan in full." - Dixie Auto Loans [6]

Lenders pay close attention to a co-signer’s financial health when determining loan terms. They’ll review the co-signer’s credit score and income to decide on approval and interest rates. In Canada, most lenders require co-signers to have a credit score between 680 and 700 [5]. They also prefer a debt-to-income (DTI) ratio below 36%, though some may consider up to 50% [5][8]. A strong co-signer can help a borrower secure interest rates between 5% and 9%, compared to rates of 10% to 15% or higher for borrowers with poor credit [5].

Legal Obligations of a Co-Signer

In Ontario, a co-signer is fully responsible for the loan, not just a portion of it [14]. If the borrower misses even one payment, the lender can legally demand the co-signer pay the full outstanding balance, including any late fees or costs associated with repossession. Once signed, vehicle purchase contracts in Ontario are legally binding, and there’s no cooling-off period that allows a co-signer to withdraw [10][11].

If the vehicle is repossessed and sold at auction for less than the remaining loan balance, the co-signer must pay the deficiency - the difference between the sale price and what’s still owed [5][13]. However, Ontario law protects borrowers and co-signers in certain situations: Once two-thirds of the loan has been paid off, the lender needs a court order to repossess or sell the vehicle [10]. Co-signers also have the option to make payments directly to bring the loan current and avoid default, but they can’t take ownership of or sell the vehicle unless they become the sole owner [5].

How Co-Signing Affects Credit Scores

Every loan payment - whether it’s on time, late, or missed - affects the co-signer’s credit score, as it’s recorded on their credit history [5][12]. A single late payment of 30 days can drop a co-signer’s credit score by more than 100 points [5]. Additionally, the total loan amount is included in the co-signer’s DTI ratio, which can limit their ability to qualify for other credit, like mortgages or personal loans [5][14].

Data from the US Federal Trade Commission reveals that 50% of bank co-signed loans and 75% of finance company co-signed loans end up requiring the co-signer to step in and make payments [14]. Because of this, co-signers should monitor the loan account themselves rather than relying solely on updates from the primary borrower [9]. While on-time payments may slightly boost the co-signer’s credit score, the added debt can still make it harder for them to borrow in the future [5][8].

When Do You Need a Co-Signer for a Car Loan in Ontario?

Lenders may ask for a co-signer when they see your financial situation as too risky for loan approval. This usually happens if you have credit challenges or a low income. Understanding these financial gaps is key to figuring out if you’ll need a co-signer for an auto loan in Ontario.

The main reasons for needing a co-signer boil down to two factors: credit issues and income challenges. Both raise concerns about your ability to make regular payments, and a co-signer with stronger finances helps ease those concerns.

Poor Credit or No Credit History

If your credit score is below 650 or you don’t have any credit history, Ontario lenders are more likely to require a co-signer. Missed payments, high credit card balances, or past defaults make lenders hesitant to approve your loan.

"Lenders often view no credit the same way they view bad credit: as a risk." – Ben Steffler, Senior Growth Manager, Clutch [4]

Not having a credit history can be just as problematic. This is common for first-time buyers, students, recent graduates, or newcomers to Canada who haven’t built a credit record yet [2][4]. Without a repayment history, lenders can’t gauge how reliable you’ll be. Most Canadian lenders expect co-signers to have a credit score of at least 650, though some prefer scores as high as 750 for higher-risk situations [1][15]. A strong co-signer doesn’t just help with approval - it can also lower your interest rates. Instead of paying subprime rates that might exceed 20%, a co-signer could help you secure rates closer to 7.99% [1].

Unstable or Low Income

Even if your credit is solid, a low or unpredictable income can lead lenders to require a co-signer. This is especially true for car loans, where amounts often exceed $50,000 [1]. If your income isn’t enough to cover monthly payments, a co-signer can strengthen your application [3].

Income instability is another red flag. For instance, if you work in commission-based sales, hospitality, seasonal jobs, or as a self-employed contractor, your monthly income might vary significantly [4][16]. Even if you earn a good annual income, lenders worry about whether you’ll have enough cash flow during slower months to keep up with payments. Self-employed individuals in Ontario should be ready to provide at least three years of tax returns to prove income stability [1]. Additionally, if you’re carrying a lot of debt - like student loans or high credit card balances - your debt-to-income ratio might be too high. In such cases, a co-signer with a lower debt-to-income ratio can help balance your application [3][4].

Next, we’ll explore the differences between a co-signer and a co-buyer.

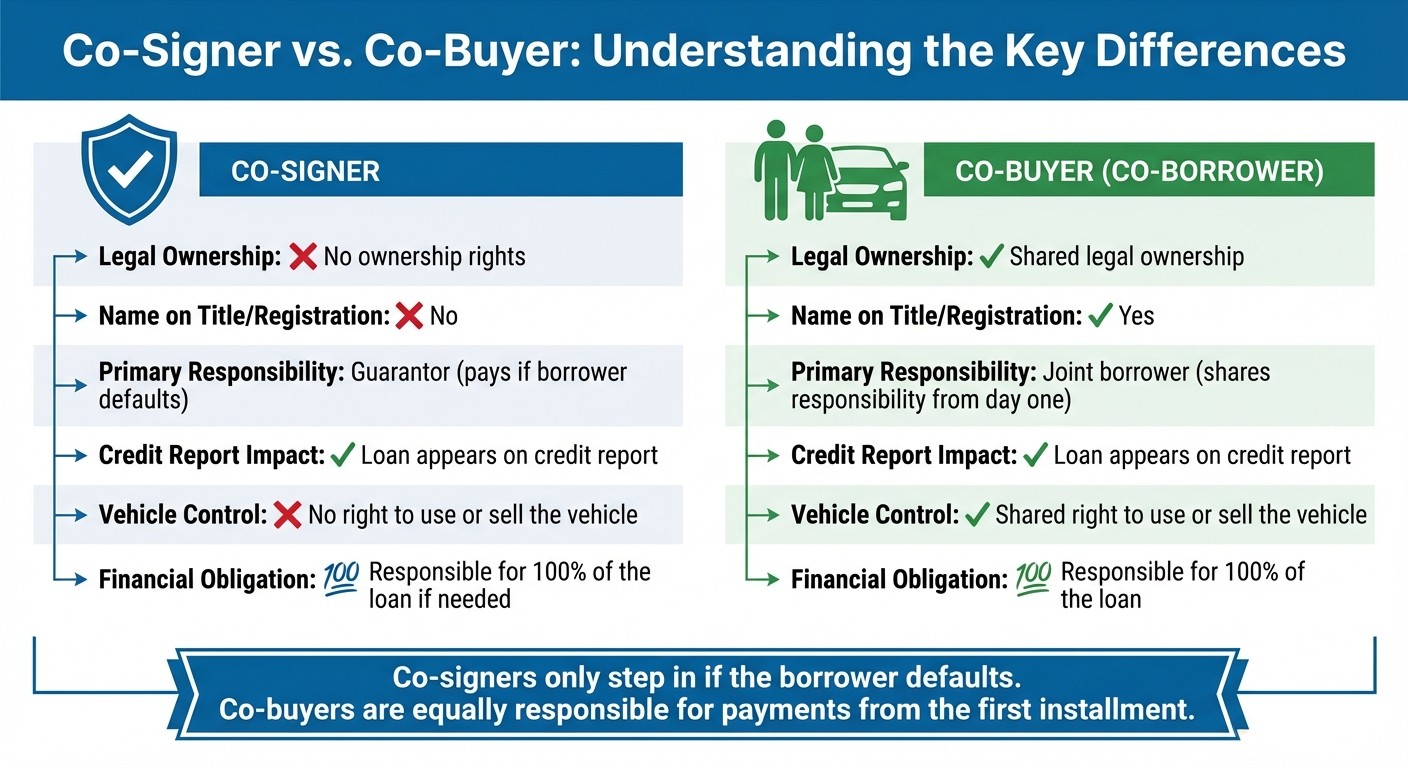

Co-Signer vs. Co-Buyer: Key Differences

Co-Signer vs Co-Buyer Comparison for Ontario Car Loans

If you're navigating auto financing in Ontario, it's crucial to understand the roles of co-signers and co-buyers. While both take on legal responsibility for a car loan, they differ significantly when it comes to ownership rights and financial expectations. Knowing these distinctions will help you decide which arrangement suits your needs.

A co-signer acts as a financial backer but does not gain any ownership rights to the vehicle. Their name is not included on the title or registration, meaning they have no legal authority to drive or sell the car. However, they are fully responsible for the loan if the primary borrower fails to make payments.

On the other hand, a co-buyer (or co-borrower) shares both financial responsibility and legal ownership of the vehicle from the start. Their name is listed on the loan agreement, the vehicle's title, and its registration. As Car Nation Canada explains, "A co-borrower is also an owner of the vehicle and shares equal responsibility for the loan from the start, regardless of whether the other borrower makes payments." Co-buyers typically share the vehicle, often seen among spouses or partners, and have full rights to use or sell it.

The key difference lies in their financial roles: co-signers only step in if the borrower defaults, while co-buyers are equally responsible for payments from the first installment. In both cases, the loan obligation is reported on their credit histories, and each party is liable for the entire loan amount.

Comparison Table: Co-Signer vs. Co-Buyer

Here's a quick breakdown to highlight the differences:

Feature | Co-Signer | Co-Buyer (Co-Borrower) |

|---|---|---|

Legal Ownership | No ownership rights | Shared legal ownership |

Name on Title/Registration | No | Yes |

Primary Responsibility | Guarantor (pays if borrower defaults) | Joint borrower (shares responsibility from day one) |

Credit Report Impact | Loan appears on credit report | Loan appears on credit report |

Vehicle Control | No right to use or sell the vehicle | Shared right to use or sell the vehicle |

Financial Obligation | Responsible for 100% of the loan if needed | Responsible for 100% of the loan |

Risks and Considerations for Co-Signers

Co-signing a car loan in Ontario is more than just a favor - it’s a serious financial commitment that can affect your credit and borrowing capacity. Before agreeing to help someone secure financing, it’s crucial to fully understand the potential risks and responsibilities involved.

Impact on Credit and Debt-to-Income Ratio

When you co-sign a loan, the entire debt is reflected on your credit report, as if it were your own. This directly impacts your debt-to-income (DTI) ratio, which lenders usually prefer to keep below 36% [5]. The full loan payment is added to your DTI, even if the borrower makes every payment on time. This could limit your ability to qualify for future loans.

In Ontario, auto loans can extend up to 84 months (seven years), meaning the financial obligation could weigh on your credit profile for a long time [5]. And if the borrower misses payments, the consequences for your credit could be significant.

What Happens If the Borrower Defaults

If the primary borrower fails to make a payment, you become immediately responsible for covering the entire loan balance, including interest, fees, and any additional collection or legal costs [21].

The damage to your credit can be severe. A single 30-day late payment could lower your credit score by more than 100 points [5]. To make matters worse, even though you’re financially liable for the debt, you don’t gain any ownership rights to the vehicle [18][16].

As George Iny, a consumer advocate with the Automobile Protection Association, warns:

"Cosign only if you can afford to take the loss on a repossession or are prepared to pay for the vehicle as a gift to the person you are guaranteeing" [19].

For instance, in 2025, a co-signer was left paying $700 per month after the primary borrower defaulted on a $62,533 car loan, and the vehicle was no longer drivable [19].

Getting out of this commitment is almost impossible without the borrower refinancing the loan [18][20]. Before signing, ask the lender if they provide a "co-signer release" option, which might allow you to be removed after the borrower makes a set number of consecutive on-time payments [20]. To protect yourself, regularly monitor the loan account to ensure payments are made on time [18][20].

How to Co-Sign a Car Loan in Ontario

Co-signing a car loan isn’t just about adding your name to a document - it’s a financial commitment that requires careful consideration. Before taking this step, it’s important to understand the process and what it entails. Here's a guide to help you navigate the co-signing process while minimizing risks.

Steps to Co-Sign a Car Loan

Start by having an open and honest conversation with the primary borrower about their financial situation. Take a close look at their income and expenses, factoring in costs like insurance, fuel, and maintenance. This will help you assess whether they can realistically afford the car without relying on your financial support.

Next, check your own eligibility. Lenders typically look for a credit score of 680 to 700, though a score above 700 can help secure more favorable interest rates [5]. Your debt-to-income ratio should ideally be below 36% and must not exceed 50% [8]. It’s also a good idea to review your credit report through services like Equifax or TransUnion to ensure there are no errors [7].

Carefully review the loan terms before signing. Pay close attention to the interest rate, repayment schedule, loan duration, and any penalties for late or missed payments [5]. In Canada, joint borrowers are entitled to receive the same disclosure details as the primary borrower, including information on interest costs and ongoing statements [22].

When it’s time to apply, both you and the primary borrower will need to submit the required documents so the lender can assess your creditworthiness, employment status, and income. Be sure to read the entire loan agreement thoroughly, especially the clauses related to default. Keep in mind that as a co-signer, you are fully responsible for the loan if the primary borrower fails to make payments [14].

Documents Required from Co-Signers

Lenders require detailed documentation to evaluate your financial stability. You’ll need to provide a valid government-issued ID, such as a driver’s license or passport, along with your Social Insurance Number for a credit check [15][25].

For income verification, gather recent pay stubs (covering at least 30 days), the previous year’s T4 slip, or your latest Notice of Assessment from the Canada Revenue Agency [5][24]. If you’re self-employed, you’ll need two years of Notice of Assessment records, along with supporting documents like business licenses, client invoices, or proof of your business website [24].

Additionally, prepare three to six months of bank statements to demonstrate consistent cash flow. You’ll also need proof of residency, which could be a utility bill, lease agreement, or mortgage statement [15][24]. Finally, a Letter of Employment confirming your job title, salary, and tenure will also be required [5].

How Hello Motors Helps Co-Signers

Once you’ve gathered the necessary documents and understand your responsibilities, it’s worth exploring how Hello Motors can simplify the process.

Hello Motors specializes in helping customers with unique credit situations, including those who require co-signers to secure financing. They offer an online pre-approval process that makes it easier for both borrowers and co-signers to evaluate their options before stepping into a dealership [3].

By partnering with various lenders, Hello Motors can provide flexible financing solutions for a range of credit profiles [3]. They assist both parties by clearly outlining the required documents and guiding you through the application process. After approval, Hello Motors reports on-time payments to credit bureaus, which can help the primary borrower rebuild their credit over time. This could eventually allow them to refinance the loan in their name, releasing you from your co-signer obligations [2].

To protect your credit score, consider requesting access to the online loan account or asking for monthly statements to be sent directly to you [23]. This way, you can monitor payments and address any issues immediately, ensuring your financial standing remains intact.

Conclusion

Co-signing a car loan in Ontario means taking on full responsibility for the debt, even though you typically don’t gain any ownership rights to the car. This decision also impacts your debt-to-income ratio, which could make it harder to qualify for other loans down the road [8]. It’s crucial to weigh all potential risks before committing.

Before stepping into the role of a co-signer, have an honest conversation with the borrower about their ability to repay the loan. As VI Drives puts it, "A good rule of thumb is to only co-sign for someone that you would lend money to" [17]. It’s also wise to ensure your credit score falls between 650 and 700 [1][5] and that your debt-to-income ratio stays below 36% [8].

Understanding the difference between co-signers and co-buyers is equally important. Only co-buyers share ownership of the vehicle, while co-signers are financially liable without ownership [26]. If you need to remove yourself as a co-signer later, the primary borrower will likely need to refinance the loan in their own name once their credit improves [26].

At Hello Motors, we’re here to simplify the car loan process for both borrowers and co-signers. Whether you’re helping someone secure financing or navigating the responsibilities of co-signing, staying informed and vigilant is key to protecting your financial well-being.