Spot red flags for odometer rollbacks, title washing, VIN cloning, curbstoning and fake listings — plus steps to verify VINs, titles, inspections, and loans.

Published Date:

6 janv. 2026

Last Updated:

6 janv. 2026

How to Spot Auto Fraud Before Buying

Auto fraud can cost you thousands of dollars and even put you at risk of buying unsafe or stolen vehicles. Common scams include odometer rollbacks, title washing, VIN cloning, curbstoning, fake listings, and misleading financing practices. These tactics often result in overpaying for cars with hidden defects or, worse, vehicles that don’t even exist. Here’s what you need to know to protect yourself:

Odometer Fraud: Over 450,000 cars with altered mileage are sold annually, costing U.S. buyers more than $1 billion.

Title Washing: Scammers erase damage histories like flood or salvage titles by exploiting state DMV loopholes.

VIN Cloning: Stolen cars are given fake identities using VINs from legitimate vehicles.

Curbstoning: Unlicensed sellers pose as private owners to offload defective or unsafe cars.

Fake Listings: Fraudulent ads lure buyers with unrealistically low prices, demanding untraceable payments.

To avoid falling victim, research sellers, verify VINs and titles, check vehicle history reports, and insist on test drives and independent inspections. When financing, review all loan terms carefully and avoid untraceable payment methods like wire transfers or gift cards. If something feels off, stop the transaction immediately and report it to authorities. Taking these steps can save you money, time, and trouble.

Police Officer Reveals How to Avoid Car Buying Scams in 2025

Common Types of Auto Fraud

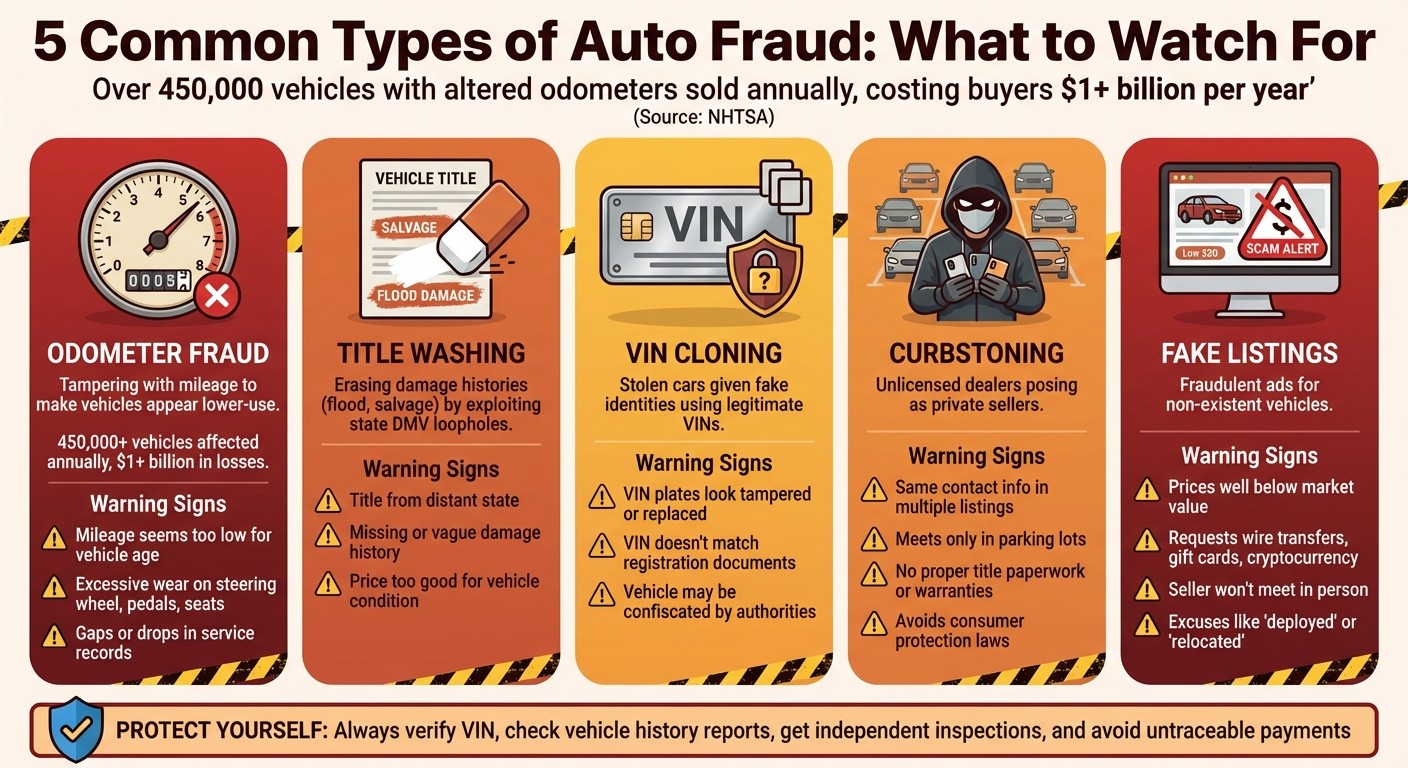

5 Common Types of Auto Fraud and Warning Signs

Knowing the most common types of auto fraud can help you spot red flags before making a purchase. While these scams vary in method, they all aim to mislead buyers - either to extract more money or to cover up serious issues. Here’s a closer look at some of the most common schemes and their risks.

Odometer Rollbacks and Mileage Fraud

Odometer fraud involves tampering with a vehicle's mileage to make it appear lower than it actually is. On older cars, scammers might physically roll back mechanical odometers, while on modern vehicles, they use electronic tools or even replace the instrument cluster to alter digital readings. Despite advancements in technology, this scam remains widespread.

The financial impact is staggering. The NHTSA estimates that over 450,000 vehicles with altered odometers are sold annually, costing buyers in the U.S. more than $1 billion every year. Lower mileage allows sellers to inflate the car’s price significantly while masking wear and tear. This deception often leads to unexpected mechanical failures and expensive repairs because the vehicle’s maintenance history doesn’t match its actual condition. In some cases, these hidden issues can even pose safety risks.

Title Fraud and VIN Tampering

Title fraud occurs when sellers manipulate a car’s title to hide serious problems like salvage branding, flood damage, or outstanding liens. One common tactic, known as title washing, involves transferring the car to a different state or altering paperwork to erase branded information such as "salvage" or "rebuilt." This loophole exploits differences in state DMV systems, making a severely damaged car appear clean to unsuspecting buyers.

VIN cloning is another dangerous scheme where scammers copy the VIN (Vehicle Identification Number) from a legitimate car and apply it to a stolen or heavily damaged vehicle. They replace VIN plates, stickers, and registration documents to give the stolen car a “clean” identity. If authorities discover the fraud, the car may be confiscated, leaving you not only without the vehicle but also dealing with legal issues and difficulties in securing insurance or resale options.

Curbstoning and Unlicensed Dealers

Curbstoning happens when unlicensed dealers pose as private sellers to dodge regulations and avoid consumer protection laws. These individuals often advertise multiple vehicles under different names or phone numbers and meet buyers in informal locations like parking lots. They rarely provide proper title paperwork or warranties, leaving buyers vulnerable.

Because curbstoners operate outside dealership rules, buyers lose access to key protections like disclosure requirements, implied warranties, and state "Lemon Law" coverage. These sellers often unload cars with hidden damage, rolled-back odometers, or washed titles - vehicles that legitimate dealers would refuse to sell. Purchasing from a curbstoner can leave you with an unsafe car that’s difficult to insure or resell.

Fake Listings and Non-Existent Vehicles

Fake listings involve fraudulent ads for cars that either don’t exist or aren’t owned by the seller. These scams often feature prices well below market value to create urgency. Scammers typically request upfront payments or deposits through wire transfers, Zelle, cryptocurrency, or gift cards - methods that are hard to trace or reverse.

These fraudsters often fabricate excuses to prevent buyers from seeing the car in person, citing reasons like deployment or relocation. Once payment is sent, the scammer vanishes, leaving the buyer with no car and no way to recover the money. Some scammers go further by collecting personal information, like Social Security numbers or banking details, under the pretense of “financing” or “verification,” which can lead to identity theft.

Misleading Financing Practices

Misleading financing practices are another common issue, often involving bait-and-switch tactics, hidden fees, and unnecessary add-ons. For example, a dealer might advertise low-interest rates or affordable monthly payments but switch to higher rates or longer loan terms without full disclosure. Contracts may also include inflated costs for warranties, GAP insurance, or other extras that significantly increase the final price.

These predatory tactics often target buyers with poor credit, pushing them into loans with high interest rates, extended terms (sometimes up to 84 months), and negative equity rollovers. This leaves buyers “upside down” - owing more than the car is worth - and at greater risk of default or repossession. To avoid these pitfalls, work with lenders or dealerships that are transparent about loan terms and allow you to review contracts thoroughly before signing.

How to Spot Auto Fraud Before You Buy

Knowing the common types of auto fraud is only the first step. To truly protect yourself, you need to dig deeper into the seller’s credibility and the vehicle’s history. A little extra effort upfront can save you thousands of dollars and spare you from legal troubles down the road.

Research the Seller and Vehicle Listing

Start with the seller. Search their contact information online along with terms like "scam" or "reviews." You can also check the Better Business Bureau for complaints. If you spot the same contact details appearing in multiple listings, it could be a curbstoning scam - a tactic where a dealer poses as a private seller.

Next, compare the asking price to the fair market value using resources like Kelley Blue Book or Edmunds. If the price is suspiciously low for the car’s year, make, model, and mileage, proceed with caution. Pay close attention to the listing itself. Look for clear details, including the VIN, current mileage, and high-quality photos of the car’s exterior, interior, odometer, and title. Be wary of vague descriptions, stock images, or inconsistencies in the vehicle’s features. If the seller refuses to provide the VIN or tries to rush your decision, consider it a red flag.

Check the VIN, Title, and Vehicle History

Once you have the VIN, run a report through services like NMVTIS, Carfax, or AutoCheck. These reports reveal crucial details like title brands (e.g., salvage, flood, rebuilt), accident history, odometer readings, and ownership records. Be alert for gaps in the history, sudden mileage drops, or a seller unwilling to provide this information. If anything seems off, it’s better to walk away.

You should also contact your state DMV or use its online tools to verify the title’s status, any brands, and active liens. Scammers sometimes use "washed" titles from other states to hide a vehicle’s troubled past. Once you’ve confirmed the history, review the documents carefully for any inconsistencies.

Look for Odometer and Wear Mismatches

Mileage can tell you a lot about a car’s true condition. On average, cars accumulate 12,000–15,000 miles per year. For instance, a ten-year-old car with just 30,000 miles should raise questions unless the seller can provide detailed maintenance records to back it up. Excessive wear on the steering wheel, pedals, driver’s seat, or carpeting in a low-mileage car might indicate odometer tampering.

Service records are another key piece of the puzzle. Look for consistent mileage entries over time. Sudden drops or unexplained gaps could signal an odometer rollback. According to the NHTSA, roughly 450,000 vehicles with altered odometers are sold annually in the U.S. [1]. To be safe, consider hiring a mechanic to inspect the instrument cluster for signs of tampering.

Review All Documents Carefully

Make sure the name on the title matches the seller’s ID. If the seller claims to be acting on behalf of someone else and their name isn’t on the title, that’s a major warning sign. The title should also clearly indicate the vehicle’s status - whether it’s salvage, rebuilt, junk, or flood. This information must be disclosed and should reflect in the price.

Check the lien section of the title as well. If a lien is listed, it means a bank or finance company still has a claim on the vehicle. The seller must provide a lien-release letter or payoff statement to ensure you can obtain clear ownership. Be cautious of titles from faraway states or those with visible alterations, mismatched VINs, or sellers unwilling to complete the transfer at a DMV or bank.

Get a Test Drive and Independent Inspection

Never agree to buy a car without a test drive and inspection. If the seller claims the car is "not accessible" but demands immediate payment, it’s almost certainly a scam. During the test drive, verify that standard warning lights (e.g., check engine, ABS, airbag) illuminate briefly when the car starts.

Drive on both city streets and highways, listening for unusual noises from the engine, transmission, or suspension. Check that the car handles well, brakes smoothly, and tracks straight. Inside, inspect for signs of prior airbag deployment, like rippled covers or misaligned seams, and test all electronics, including windows, locks, and the infotainment system.

Before finalizing the deal, arrange for an independent pre-purchase inspection with an ASE-certified mechanic who has no connection to the seller. A thorough inspection should cover frame damage, rust, fluid leaks, diagnostic trouble codes, and signs of prior collisions or flood damage. Mechanics often uncover hidden issues like unrepaired accident damage, corrosion from floods, or wear that doesn’t match the car’s reported mileage. If the seller resists an independent inspection or tries to pressure you into skipping it, that’s a clear sign to walk away.

Protecting Yourself in Auto Financing

Financing fraud can turn what seems like a great deal into a financial disaster. Even if the car itself meets your expectations, some dealers and lenders may inflate costs, sneak in hidden fees, or impose unfair loan terms. Knowing how to thoroughly review your loan documents and identify potential red flags is just as critical as inspecting the vehicle itself.

Review Loan Terms and Disclosures

Before signing any agreements, demand the full price in writing - this includes the car's cost, taxes, and fees. Compare this total to the principal amount listed in your loan contract. If there’s a large, unexplained difference, it could indicate hidden markups.

Pay close attention to the Truth in Lending Act (TILA) disclosure. This document is key and should clearly outline the annual percentage rate (APR), finance charges, total loan amount, payment schedule, and any penalties for early payoff. Cross-check these numbers against any advertised rates or figures provided by the dealer. If the TILA disclosure doesn’t match up, you could be dealing with a bait-and-switch tactic.

For example, if you’re borrowing $15,000 at a 5% APR over 60 months, your monthly payment should be around $283. Use an online loan calculator to verify this. If the numbers don’t add up, ask for clarification or walk away from the deal. Also, carefully examine any extra fees or add-ons before finalizing the loan.

Avoid Unnecessary Add-Ons and Fees

Dealers often push extended warranties, GAP insurance, and other extras as though they’re essential. They’re not. These add-ons can be heavily marked up. For instance, GAP insurance - which covers the difference between your loan balance and the car's value if it’s totaled - might cost $300-$600 through your insurance provider but could be priced at $1,000 or more at the dealership.

If you’re not interested in these extras, ask for a revised contract with all add-ons removed. Then, compare the updated pricing. If the dealer refuses or insists these items are non-negotiable, consider it a major red flag. You have the right to decline these products in writing. For fair pricing, consult independent sources like AAA or Consumer Reports. For example, extended warranties typically range between $1,200 and $2,500 for five years of coverage. If the price is significantly higher, you’re better off negotiating or buying from a third-party provider after the sale.

Lastly, ensure all payment methods are secure and traceable to protect yourself from scams.

Watch Out for Payment Scams

Avoid untraceable payment methods like wire transfers, cryptocurrency, or gift cards when buying a car. These are common tools for scammers. In one case, a buyer in California lost $82,000 after wiring money to what appeared to be a legitimate dealership in Indiana - only to find out it didn’t exist. Wire transfers and gift cards are nearly impossible to reverse, which is why fraudsters prefer them.

Stick to secure payment options like cashier’s checks issued at the dealership, credit cards (which offer dispute protections under federal law), or direct bank transfers completed in person. If a seller suggests using a specific escrow service, verify its legitimacy through its official website. Be cautious of "overpayment" scams, where you’re sent a check for more than the agreed amount and asked to refund the difference via wire transfer. The original check will inevitably bounce, leaving you on the hook for the money you sent back.

What to Do If You Suspect Fraud

Stop the Transaction Immediately

If you notice anything suspicious, don’t waste time - take immediate action. Cancel the transaction right away if you spot any warning signs. Avoid signing documents, transferring funds, or sharing personal information. Red flags could include unrealistically low prices, sellers refusing in-person inspections, or paperwork that doesn’t add up.

If you’ve already sent money through wire transfer, ACH, or Zelle, contact your bank or payment provider immediately to try to recall the payment or file a fraud claim. Acting quickly gives you a better chance of recovering your funds.

Report Fraud to the Proper Authorities

Gather and organize all the evidence related to the transaction. Save screenshots of online listings, emails, text messages, and any written agreements or pricing details. Keep copies of important documents like bills of sale, financing paperwork, and vehicle history reports to highlight any discrepancies.

Here’s where to report fraud:

State DMV: If you suspect issues like odometer tampering, title washing, VIN cloning, or a stolen vehicle, notify your state DMV.

State Attorney General’s Office: For deceptive sales practices, bait-and-switch tactics, or unfair financing terms, file a complaint with your state Attorney General.

Federal Trade Commission (FTC): Report unfair or deceptive vehicle sales and financing practices at ftc.gov.

Local Law Enforcement: If the seller has taken your money and vanished, file a police report with your local authorities.

National Highway Traffic Safety Administration (NHTSA): For safety-related defects or significant undisclosed damage (like flood or frame damage), report the issue to NHTSA. According to NHTSA, odometer fraud alone costs American car buyers over $1 billion every year [2].

Once you’ve reported the fraud, stick to dealing with verified and trustworthy sources.

Work with Reputable Dealerships

To protect yourself in the long run, stick to licensed and well-established dealerships. Check the dealer’s license through your state DMV or Attorney General’s office, and read online reviews, Better Business Bureau ratings, and complaint histories to assess their reputation.

Reputable dealerships are transparent about a vehicle’s history, including prior accidents or title issues. They’ll encourage independent inspections and won’t pressure you to skip a pre-purchase check. They’ll also clearly explain financing terms, fees, and any additional costs before you sign anything. Trusted dealerships, like Hello Motors, provide detailed vehicle histories, support independent inspections, and clearly outline financing terms, helping to minimize fraud risks.

Conclusion

Buying a used car doesn’t have to feel like a risky gamble if you know what to look for and take the right precautions. Odometer fraud alone costs American buyers over $1 billion each year, according to the National Highway Traffic Safety Administration [2]. But here’s the good news: most scams can be avoided if you take the time to verify the details. Start by running a VIN-based history report, cross-checking mileage with wear and service records, taking the car for a test drive, and getting it inspected by a trusted mechanic. These steps can help you identify fraud schemes like title washing, VIN cloning, fake listings, or curbstoning.

When it comes to finances, read every line of your paperwork carefully. Avoid risky payment methods like wire transfers, gift cards, or cryptocurrency. If a seller pressures you to skip inspections, refuses to meet face-to-face, or offers a deal that seems too good to be true, trust your instincts and walk away. Saying no to suspicious offers is one of the best ways to protect yourself.

At the first sign of trouble, stop the transaction immediately and report it to the FTC, your state DMV, and local law enforcement. Save all evidence, including screenshots, emails, texts, and bills of sale, to strengthen your case.

For added peace of mind, stick to working with licensed, reputable dealerships. Trusted sellers provide transparency with clear pricing, detailed vehicle histories, and encourage independent inspections. For example, companies like Hello Motors prioritize these practices, offering verifiable vehicle histories and full financial disclosures to make your car-buying experience safer and more reliable.