Ontario has no legal minimum down payment for used cars; lenders typically recommend 10–20%. Zero-down is available but often costs more.

Published Date:

Jan 17, 2026

Last Updated:

Jan 17, 2026

Minimum Down Payment for Used Cars in Ontario

In Ontario, there’s no legal requirement for a minimum down payment when buying a used car. However, lenders and dealerships often recommend putting down 10–20% of the vehicle's price. A larger down payment can lead to:

Lower monthly payments and reduced total interest costs.

Improved loan approval chances, especially for those with lower credit scores.

Protection from negative equity, where you owe more than the car’s value.

For example, on a $20,000 car, a 20% down payment ($4,000) leaves $16,000 to finance, which helps reduce risks and build equity. While zero-down financing is available, it typically comes with higher interest rates and monthly payments. Planning your budget carefully and considering upfront costs, such as Ontario’s 13% sales tax, is essential for a smoother car-buying experience.

How Do I Finance a Car? - Down Payments, Credit Check, Monthly Payments

Is There a Legal Minimum Down Payment in Ontario?

No, Ontario does not legally require a minimum down payment for used car purchases. There’s no law setting a baseline for how much money you need to put down when buying a vehicle. Instead, the amount is entirely up to the lender or dealership providing the financing [8][9].

What the law does require is transparency. The Consumer Protection Act mandates that any down payment, along with the annual percentage rate (APR) and total borrowing cost, must be clearly outlined in your credit or lease agreement [10]. Both the Motor Vehicle Dealers Act (MVDA) and the Consumer Protection Act (CPA) prioritize full disclosure and consumer protection, rather than enforcing minimum down payment amounts [10]. This ensures that buyers are fully informed about the terms of their financing.

Deposits to hold or order a vehicle are governed by contract law, not by specific legal requirements [5]. If no contract has been signed, you’re entitled to a refund of your deposit upon request [9]. To safeguard your interests, consider adding a "subject to acceptable financing" condition to your bill of sale. This clause allows you to back out and reclaim your deposit if the lender's down payment terms don’t align with your expectations [9].

Once you’ve entered into a financing agreement, Ontario provides robust consumer protections. For instance, if you’ve paid off at least two-thirds (66.6%) of your loan, the lender cannot repossess or sell your car without obtaining a court order from the Ontario Superior Court of Justice [8]. Additionally, the Motor Vehicle Dealers Compensation Fund offers coverage of up to $45,000 for deposits or payments if a registered dealer fails to deliver your vehicle [8].

Up next, we’ll look at best practices when it comes to making down payments.

What Is the Recommended Minimum Down Payment for Used Cars?

When buying a used car, financial experts generally recommend putting down at least 10% of the vehicle’s purchase price. Since used cars have already gone through significant depreciation, this percentage helps minimize financial risks [12]. Ideally, aiming for a down payment closer to 20% can lead to even better loan terms.

Let’s break it down: if you’re purchasing a $25,000 car, 10% would be $2,500, while 20% would amount to $5,000. The higher your initial payment, the better your chances of securing favorable loan conditions.

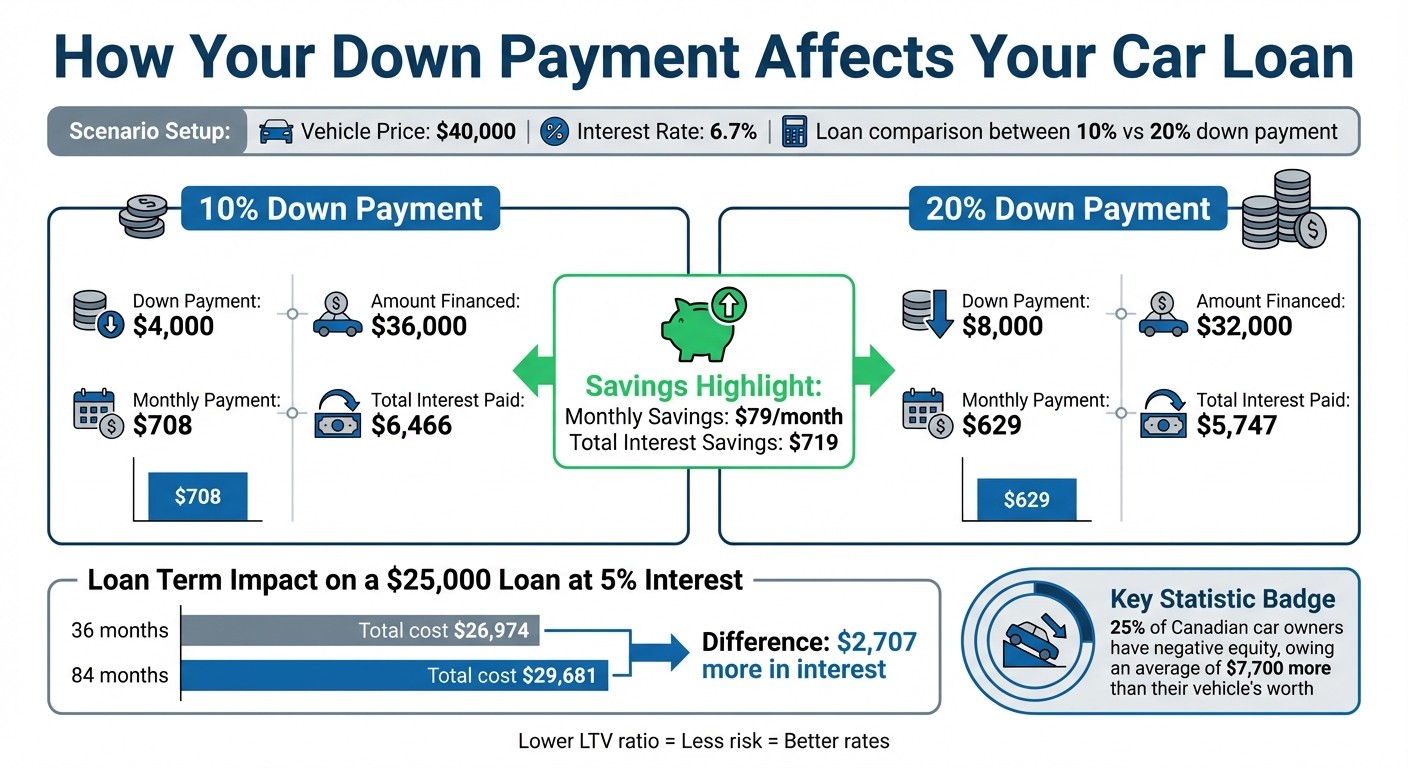

Why does this matter? A larger down payment reduces the lender’s risk, which often translates to lower interest rates and faster equity buildup. For example, on a $40,000 car with a 6.70% interest rate, putting 20% down instead of 10% can save you nearly $719 in total interest over the life of the loan [12]. It also helps you avoid negative equity - owing more on your loan than the car’s value [13].

For buyers with less-than-perfect credit, hitting that 10% minimum can be crucial. Lenders often see a solid down payment as a sign of financial responsibility, which could mean the difference between getting approved or denied for a loan. According to a study by Edmunds, the average buyer puts down 11.7% on vehicle purchases, showing that many recognize the importance of this upfront investment [14].

That said, don’t stretch your finances too thin. Rod Griffin advises keeping enough in your emergency savings to handle unexpected expenses [7].

Up next, let’s look at whether financing a used car with no down payment is a realistic option.

Can You Finance a Used Car with No Down Payment?

Yes, zero-down financing is an option in Ontario, thanks to specialized lenders and dealerships that allow buyers to finance the full cost of a used vehicle [17][6]. While it’s generally advised to put down 10% to 20%, it’s not a hard rule. Many financing programs are designed for those who either can’t or choose not to make an upfront payment.

Your eligibility for $0 down financing largely depends on your credit score and the lender’s policies [6]. If your credit score is above 630 (prime borrower), you’re more likely to qualify for zero-down approval and benefit from lower interest rates, typically between 4.99% and 8.99% [6]. For those with scores between 300 and 629 (subprime borrowers), the path can be more challenging. Many Ontario lenders require at least $500 or 5% of the vehicle’s price as a minimum down payment, along with higher interest rates ranging from 9.0% to 29.5% [6]. This is where Hello Motors steps in to offer tailored financing solutions.

Hello Motors specializes in personalized no-down-payment financing for customers across various credit profiles [16]. The process is straightforward: you complete a secure 60-second online application, and a dedicated finance manager reviews your file to provide approval options that align with your budget. Approvals are often delivered within 24 hours [16][21]. For example, in 2025, Chris Hochscheidt, a customer who had been turned down by other lenders, shared his experience with Hello Motors:

worked out everything for me to get approved when others wouldn't and now I'm driving my dream car with an amazing rate! [21]

However, zero-down financing does come with some trade-offs. Borrowing the full cost of the vehicle means higher monthly payments and more interest over the life of the loan [2]. Even with no-down-payment financing, it’s wise to have at least $500 on hand in case a token deposit is required [6]. If you own a car with equity, trading it in can count toward the down payment and may improve your chances of approval [6].

Lenders typically assess three main factors for zero-down applications: your creditworthiness, your ability to manage monthly payments (usually requiring at least $1,800 in income per month), and the fair market value of the vehicle you’re buying [18][20]. To strengthen your application, you’ll need at least three months of steady employment, valid ID, recent pay stubs, proof of residency, and banking details [19][20].

How Down Payment Size Affects Loan Terms

Down Payment Impact on Car Loan Costs in Ontario

The size of your down payment plays a big role in shaping your loan terms. A larger down payment reduces the loan principal, which can lower both your monthly payments and the total interest you’ll pay over time[13]. For instance, if you’re purchasing a $40,000 vehicle with a 6.7% interest rate, putting down $8,000 (20%) results in a monthly payment of $629 and total interest of $5,747. However, cutting the down payment to $4,000 (10%) increases the monthly payment to $708 and total interest to $6,466[12].

But that’s not all - a bigger down payment can also help you snag a lower interest rate. As Chris Hardesty from Kelley Blue Book explains:

A lower LTV ratio is viewed as less risky, so the lender may offer more favorable financing options[7].

Another factor to consider is equity. Nearly 25% of Canadian car owners are currently dealing with negative equity, owing an average of $7,700 more than their vehicle’s worth[22]. By making a substantial down payment, you create a cushion of equity that safeguards you as your car depreciates. This can be especially important if your vehicle is stolen or totaled, as insurance payouts based on market value are more likely to cover the remaining loan balance[3].

The loan term you choose also has a big impact. For example, a $25,000 loan at 5% interest would cost $26,974 over 36 months, compared to $29,681 over 84 months - a difference of $2,707 in total interest paid[5]. Larger down payments can make shorter loan terms more manageable. Jeff Donnelly, Chief Consumer Protection Officer at OMVIC, cautions:

Long-term loans are enticing because they may allow you to buy something you normally can't afford, even if you can make the monthly payment[23].

Ultimately, these factors highlight why your down payment size is a key piece of the puzzle when it comes to crafting the best financing plan for your vehicle.

Factors That Determine Down Payment Requirements

Several key factors influence how much of a down payment you'll need when financing a vehicle. Let’s break them down to better understand the role each plays.

Your credit score is a major factor. In Ontario, most lenders look for a score of 650 or higher [24]. If your score is below this, you might need to put down more money upfront. For those with a score under 580, lenders often require a down payment of 20% or more to approve the loan [12]. As Lisa Rennie, Senior Contributor at Loans Canada, points out:

Some lenders may still require a down payment on a car, especially if you have poor credit [3].

Another important consideration is your debt-to-income (DTI) ratio. This measures how much of your monthly income goes toward paying off debts. A lower DTI - ideally 32% or less - makes your financing application stronger. On the other hand, a DTI above 50% can make finding approval more challenging [17][25]. A larger down payment can help here by reducing the loan amount, which in turn lowers your monthly payments and improves your DTI.

Your income level also plays a role. Lenders evaluate whether your income can comfortably handle the monthly car payments. Many follow the "20/4/10 rule", which suggests a 20% down payment, a four-year loan term, and limiting total transportation costs to 10% of your monthly income [15].

If you have a trade-in, it can help reduce the down payment needed. The equity from your current vehicle is applied toward the lender's minimum down payment requirements [1][3]. Plus, in Ontario, you only pay HST on the price difference between the new vehicle and your trade-in. For instance, if you trade in a $10,000 car toward a $25,000 purchase, you could save around $1,300 in taxes [26].

Lastly, lender policies vary. Some dealerships, particularly those focused on bad credit financing, may offer more accommodating terms. In contrast, traditional banks often stick to stricter guidelines. Taking the time to shop around can help you find an option that aligns with your financial situation. Together, these factors shape your down payment requirements and influence your overall car financing strategy in Ontario.

Hello Motors Financing Options for Used Cars

Hello Motors offers flexible financing plans designed to fit a variety of budgets and credit situations. Their three main plans - Basic Financing, Premium Financing, and Custom Financing - are tailored to meet individual needs. By partnering with top Canadian auto finance institutions, they provide personalized solutions for all types of credit [21].

One standout feature is the $0 down payment option, available for those with approved credit [21]. Buyers who qualify can also defer their first payment for up to three months [21]. The application process is quick and simple: fill out a 60-second online form, and you’ll usually receive approval within 24 hours [16][21]. Once submitted, a finance manager reviews your file to offer customized options. This streamlined approach helps build trust and confidence in Hello Motors' services.

The dealership boasts an impressive 4.9 out of 5-star rating based on verified customer reviews [21]. Take the story of Chris Hochscheidt, who found success with Hello Motors after being turned down elsewhere:

worked out everything for me to get approved when others wouldn't and now I'm driving my dream car with an amazing rate! [21]

Representative Ibrahim not only managed Chris’s approval but also arranged for his car to be delivered directly to his home [21].

Hello Motors goes beyond financing by offering additional services to enhance your car-buying experience. If the specific vehicle you’re looking for isn’t available, they can locate it for you through their vehicle sourcing service. For example, business owner Dan Mathieson worked with Ibrahim to find a truck that fit his strict monthly budget, and it was delivered to his doorstep in just a few days [21]. Their home delivery service covers all of Ontario, making it possible to complete the entire purchase process without leaving your home.

To get started, make sure you have your valid driver’s license, proof of residence, and income documentation ready. These documents help speed up the approval process and allow your finance manager to present the best options for your situation.

Conclusion

In Ontario, there isn’t a legal minimum down payment required for buying a used car. Instead, lenders and dealerships set their own terms based on your credit and financial situation [27][4]. While $0 down financing is an option, many experts suggest putting down 10%–20% to make the purchase more manageable [27][11][2].

Making a larger down payment can lead to lower monthly payments, reduced interest costs, and better chances of loan approval. Even setting aside $2,000 to $5,000 can make a noticeable difference. Don’t forget to account for Ontario’s 13% sales tax as part of your budget [28][2][4]. These factors highlight the importance of planning your down payment carefully before diving into financing options.

Hello Motors offers flexible financing tailored to your credit situation, including a $0 down option and quick online approvals. With three customizable financing plans and partnerships with leading Canadian lenders, they help you find a payment plan that fits your budget and needs.

Once you’ve explored financing options, the next step is preparing your documentation. Check your credit score and gather key documents like your driver’s license, proof of residence, and income verification. Getting pre-approved can clarify your budget and give you more confidence when negotiating [27][15]. Whether you choose to make a down payment or opt for zero-down financing, aim to keep your monthly car expenses below 10% of your gross monthly income [28][15]. Planning ahead ensures a smoother, more confident car-buying experience.