Understand APR vs interest rate, what affects your auto loan APR, where it appears in contracts, and practical tips to compare or lower financing costs.

Published Date:

Dec 17, 2025

Last Updated:

Dec 17, 2025

Understanding APR in Auto Financing Agreements

When financing a car, the Annual Percentage Rate (APR) is one of the most critical factors to consider. It reflects the total yearly cost of borrowing, including both the interest rate and additional fees. APR helps you understand the true cost of your loan, ensuring you can compare offers fairly and avoid hidden expenses. Here's what you need to know:

APR vs. Interest Rate: APR includes extra fees like origination or application charges, while the interest rate only reflects the cost of borrowing.

Impact on Costs: A 1% reduction in APR on a $25,000 loan over 48 months can save you over $400 in interest.

What Affects APR: Your credit score, down payment, loan term, and vehicle type all influence the rate you're offered.

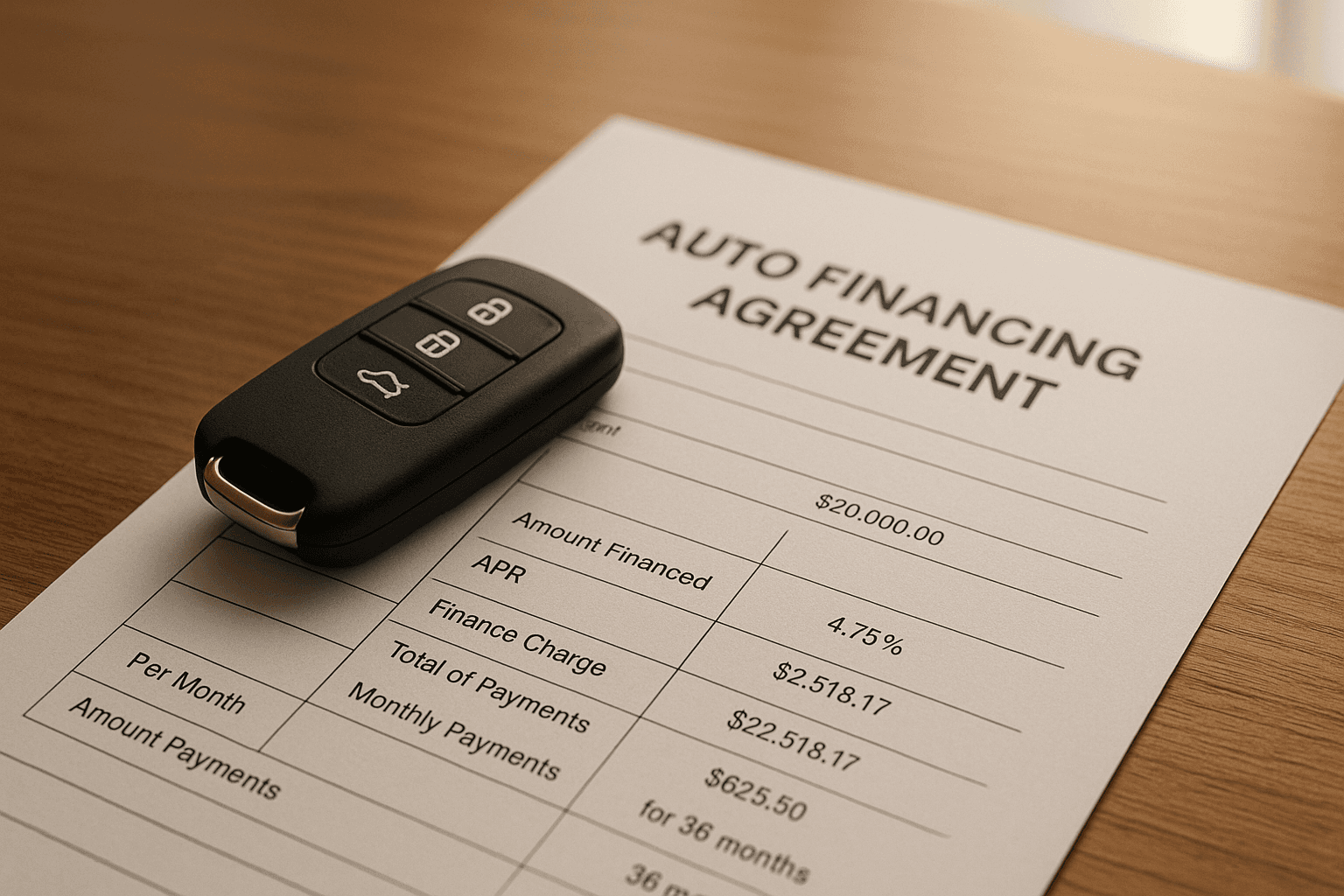

Where to Find APR: It's disclosed in your loan agreement, typically in the "Finance Charge" or "Summary of Terms" section.

Understanding APR ensures you avoid costly mistakes, compare loans accurately, and make informed decisions. Always review your contract for hidden fees and discrepancies before signing.

Car Loans - What's the difference between an Interest Rate & APR?

What is APR and Why Does It Matter?

APR, or Annual Percentage Rate, is the yearly cost of borrowing money for an auto loan, expressed as a percentage. Unlike the interest rate, which only accounts for the cost of borrowing, APR includes additional fees tied to the loan, like origination charges, application fees, or processing costs. This makes it a more accurate reflection of what you're actually paying to finance your vehicle.

When comparing loan offers, focusing solely on the interest rate can be misleading. For instance, a lender might promote a 5% interest rate, which sounds appealing. But if there are extra fees bundled into the loan, the actual cost of borrowing could be much higher. APR combines the interest rate with these fees into one annualized percentage, giving you a clearer picture of the total cost.

Federal law requires lenders to disclose APRs. This transparency allows you to compare loan options more easily. Since APR factors in additional fees, it’s usually higher than the stated interest rate. For borrowers with excellent credit and minimal fees, the two rates might be close. However, when upfront or hidden charges are involved, the APR rises, signaling a more expensive loan overall.

Using APR as your main comparison tool helps you avoid loans that appear cheap on the surface but come with costly fees. Instead of being swayed by catchy phrases like "low rate" or "easy approval", you can focus on the actual cost of borrowing. Understanding APR sets the stage for evaluating how it differs from the nominal interest rate and how it impacts your auto loan.

APR vs. Interest Rate: What's the Difference?

The interest rate is the base cost of borrowing money, while the APR includes both the interest rate and certain mandatory fees, expressed as an annual percentage.

For example, if a dealer offers a 6% interest rate but adds a $500 origination fee and a $300 processing fee, the APR might increase to around 6.5% or 6.8%. This shows the true cost of borrowing, beyond just the interest.

It’s worth noting that optional add-ons, like extended warranties or GAP insurance, aren’t typically included in the APR calculation. However, financing these extras increases the total loan amount, meaning you’ll pay interest on them over time.

Here’s a practical takeaway: If two loans have the same monthly payment but different APRs, the one with the higher APR will cost you more in the long run. Recent data from 2023–2024 shows that average APRs for new cars hover around 7%, while used car loans tend to have even higher rates. Your credit score plays a big role too - borrowers with excellent credit might secure rates in the mid-single digits, while those with lower scores could face APRs in the mid-teens or higher. These variations highlight why understanding both interest rate and APR is essential when comparing loan offers.

How APR Affects Your Auto Loan

APR impacts both your monthly payment and the total cost of the loan. A higher APR means a larger portion of each payment goes toward interest rather than reducing the principal. Over time, even a small difference in APR can add up to hundreds - or even thousands - of dollars in extra costs.

For example, on a $25,000 loan over 48 months, reducing the APR by just 1% could save you over $400 in interest. While the monthly savings might seem small, the cumulative effect is significant.

The loan term also influences how much interest you’ll pay overall. Extending the same loan to 60 months might lower your monthly payment, but it increases the total interest paid because you’re borrowing money for a longer period. Even if the APR stays the same, a longer loan term results in higher total costs.

APR can also help you weigh trade-offs. For instance, promotional 0% APR offers on new cars often require excellent credit and may come with conditions like reduced cash rebates. In some cases, choosing a low APR with a rebate might save you more than a 0% APR offer without one. Understanding APR ensures that you’re not drawn to deals that only appear attractive at first glance.

When working with dealerships or used-car specialists offering in-house financing - especially those advertising flexible options for all credit types - APR becomes an essential tool for comparison. For example, at Hello Motors, clear APR disclosures help customers understand financing costs. Comparing dealer-arranged APRs with quotes from banks or credit unions can help you decide whether the convenience of in-house financing is worth any additional cost, or if securing your own loan is a better choice.

How APR is Calculated and Disclosed

Knowing how APR is calculated and where to find it in your contract is crucial for ensuring you agree to the terms you expect. Federal law requires lenders to disclose APR in a standardized format, giving you a clear view of the true annual cost of borrowing. Let’s break down what goes into APR and how to locate it in your loan documents.

What's Included in APR Calculations

APR, or Annual Percentage Rate, combines the interest rate with certain mandatory fees to give you a clearer picture of your loan’s total cost. It starts with the interest rate and includes fees like loan origination, application, administrative, document preparation, and prepaid interest charges. If credit insurance is a required condition of the loan, its premiums may also be factored into the APR.

Since these fees are spread out over the life of the loan, the APR often ends up being higher than the stated interest rate. For instance, financing a $25,000 car at a 3.00% interest rate with a $500 fee could lead to an APR of about 3.5%, reflecting the additional costs distributed over the loan term.

It’s important to note that optional add-ons, such as extended warranties or service contracts, are usually not included in the APR unless you choose to finance them along with the loan. Similarly, fees like annual charges or late payment penalties don’t affect the APR, though they can still impact your overall costs.

The Truth in Lending Act requires lenders to disclose both the interest rate and the APR in auto financing agreements[4]. This ensures transparency, preventing lenders from using low interest rates to mask hidden fees. Always review the fee breakdown in your contract carefully - lenders may either itemize charges or group them together, so it’s worth verifying any unusually high amounts.

Where to Find APR in Your Contract

Once you understand how APR is calculated, it’s equally important to know where to locate it in your financing documents. Typically, the APR is listed in the "Finance Charge" or "Summary of Terms" section of your auto loan agreement[4]. This section not only details the APR but also includes the interest rate, loan amount, monthly payment, and total repayment amount over the loan term. Comparing the APR in your contract with the rate quoted during negotiations can help you spot any unexpected fees that may have been added.

Be cautious if your contract only shows the interest rate, lacks a clear fee breakdown, or reveals a large gap between the quoted rate and the APR (e.g., a 5% interest rate paired with a 7% APR). Such discrepancies should prompt you to ask for clarification about which fees are driving up the APR. Reviewing these details ensures you understand the fee structure and the overall APR calculation.

Additionally, your contract will indicate whether the APR is fixed or variable. Fixed APRs remain steady throughout the loan term, while variable APRs can fluctuate based on market conditions. If you have a variable APR, your contract should clearly explain how and when the rate might change[1], giving you insight into potential risks tied to future rate increases.

Taking the time to review and verify all these details before signing can help you avoid unexpected costs and make a well-informed decision about your auto financing.

What Affects Your APR

Your APR isn’t a fixed number - it varies based on several factors. Lenders evaluate risk by looking at your financial history, the specifics of the vehicle and loan, and their own pricing policies. Let’s break down how each of these influences your APR.

Your Personal Financial Profile

Your credit score plays a major role in determining your APR. It’s essentially a snapshot of how reliable you are at managing debt. According to CARFAX data from Q1 2024, borrowers with credit scores above 781 typically saw auto loan rates around 5.38% for new cars and 6.00% for used cars. On the other hand, those with scores below 500 faced rates averaging 15.62% for new vehicles and a steep 21.57% for used ones[1]. Even a small improvement in your credit score - like moving from 680 to 740 - can lead to better loan terms.

Another key factor is your debt-to-income (DTI) ratio, which measures how much of your monthly income goes toward debt payments, including car loans, credit cards, housing, and student loans. Lenders tend to offer better rates to borrowers with lower DTIs because they have more financial breathing room. For example, two applicants with the same credit score might receive different APRs if one has a DTI of 25% while the other’s is 45%[1][4].

Income stability also matters. Lenders are more likely to offer favorable rates to borrowers with steady, documented income and a solid employment history. Some lenders even factor in how long you’ve been at your current job when determining your rate[3][4].

Lastly, the size of your down payment can directly affect your APR. A larger down payment reduces the amount you need to borrow, which lowers the loan-to-value (LTV) ratio and decreases the lender’s risk. For instance, putting 20% down on a car can significantly reduce your APR compared to financing nearly the entire purchase price[1][5].

Vehicle and Loan Characteristics

The type of vehicle and how your loan is structured also impact your APR. New cars generally qualify for lower rates than used ones because they hold their value better and are easier to resell if repossessed. Used vehicles, especially older models or those with high mileage, often come with higher APRs due to faster depreciation and potential maintenance issues. For example, Edmunds data from Q1 2023 showed the average APR for new vehicles was about 7%, a trend expected to continue for 5-year loans in 2024[1].

Within the used-car market, specifics like vehicle age and mileage matter. A three-year-old certified pre-owned sedan with 30,000 miles will likely have a lower APR than a ten-year-old truck with 120,000 miles, largely because the newer car is less risky for the lender.

Loan term length also plays a role. Shorter terms, such as 36 or 48 months, usually come with lower APRs and result in less total interest paid, though the monthly payments are higher. Longer terms - like 60, 72, or even 84 months - can reduce monthly payments but often come with higher APRs and more total interest over the life of the loan. Finding the right balance between monthly affordability and overall cost is key.

The loan-to-value (LTV) ratio is another factor. If you’re financing the full purchase price - or even more, including fees - your APR will likely be higher. Lenders see higher LTVs as riskier, which is why financing 100% or more of a vehicle’s value often comes with a steeper rate[1][2].

Lender and Dealer Pricing

Lenders set a base rate, known as the "buy rate", based on your financial profile. However, dealers often add a markup to this rate, meaning two borrowers with similar profiles could end up with different APRs depending on the dealer’s pricing policies[4][5].

Promotional APR offers, like 0% financing, are another factor to consider. These deals are often subsidized by manufacturers or dealers and typically apply to specific models or loan terms. However, they’re usually reserved for buyers with top-tier credit and may come with conditions like shorter loan terms or the loss of other incentives, such as cash rebates[1][3].

Optional add-ons and fees can also raise your effective APR. Products like extended warranties, GAP insurance, or credit insurance, when rolled into your loan, increase the overall finance charge. Similarly, fees like origination or documentation charges can make a loan with a seemingly lower interest rate end up costing more overall[1][4].

Understanding these factors gives you an edge when shopping for an auto loan. Steps like reducing existing debt, correcting errors on your credit report, saving for a larger down payment, and selecting the right loan term can all improve your chances of securing a better APR. Getting preapproved through a bank or credit union and comparing multiple offers can also put you in a stronger negotiating position with dealers[2][4]. These considerations will be even more important as we delve into comparing APRs in the next section.

How to Use APR When Shopping for Auto Loans

Understanding APR can help you make smarter decisions when comparing auto loan offers. It's not just about finding the lowest monthly payment - it’s about identifying the loan that costs you the least over time. APR serves as your go-to tool for making these comparisons.

Comparing APRs from Different Lenders

Start by gathering written APR quotes from banks, credit unions, and dealership financing. To make an accurate comparison, ensure all quotes are based on the same loan amount, term length, and down payment. For example, comparing a 60-month loan from one lender to a 72-month loan from another won’t give you a clear picture[1][2].

Ask lenders if their APR includes all fees. Some may bundle charges like origination or documentation fees into the loan, which increases the effective APR, while others list these costs separately[1][5].

A quick comparison table can help you see how APR differences add up. Let’s say you’re financing $25,000 over 60 months:

APR | Monthly Payment | Total Interest Paid | Total Cost |

|---|---|---|---|

4% | $460 | $2,600 | $27,600 |

7% | $495 | $4,700 | $29,700 |

12% | $556 | $8,360 | $33,360 |

Notice how a 4% APR saves you over $2,000 compared to a 7% APR, and nearly $6,000 compared to a 12% APR. This highlights why focusing solely on monthly payments can be misleading. A slightly higher monthly payment on a lower-APR loan could save you thousands in the long run.

Also, check for any conditions tied to the APR. Some lenders may offer discounts if you set up automatic payments or already have an account with them[1][2]. Once you’ve gathered the quotes, review them carefully for hidden fees or inconsistencies.

Warning Signs in APR Disclosures

Not all APR quotes are straightforward, so it’s important to spot potential red flags early.

If a dealer’s APR is significantly higher than your preapproved rate, dig deeper. For instance, if your bank preapproved you at 6% but the dealer offers 10% without a clear reason, it’s worth investigating[4][5].

Be cautious of high fees labeled as "doc", "processing", or "loan origination" charges. Ask for an itemized breakdown and negotiate to remove or lower these fees if they seem excessive. Similarly, watch out for optional add-ons like extended warranties, GAP insurance, or service contracts that you didn’t request. These extras increase the amount financed and can raise your effective APR. Always ask to see a version of the contract without these add-ons to clearly assess the base loan terms[1][4][5].

Review the federal Truth in Lending disclosure box on your loan contract. This section lists the APR, finance charge, total payments, and amount financed. Ensure these figures match what you were initially quoted. If discrepancies arise, address them before signing[4].

Lastly, remember that a "low" APR isn’t always the best deal. For example, a dealer may advertise 0% to 1.9% financing but require you to give up a cash rebate or extend the loan term, which could cost you more overall. In some cases, a slightly higher APR on a shorter-term loan may save you money in the end[2][4].

Spotting these red flags can help you negotiate better terms and avoid costly surprises.

How to Negotiate a Lower APR

Use your preapproval as leverage to secure a better APR. Before visiting the dealership, get preapproved by a bank or credit union and bring that written offer with you. Ask the dealer if they can match or beat the rate. Dealers often work with multiple lenders and may reduce their markup to win your business[1][5].

You can also lower your APR by increasing your down payment, choosing a shorter loan term, or setting up automatic payments. A larger down payment reduces the loan-to-value ratio, which lowers the lender’s risk[1][5]. While shorter terms may lead to higher monthly payments, they significantly reduce the total interest paid over the life of the loan[1][3]. Some lenders even offer rate discounts for automatic payments linked to your checking account.

Improving your credit profile can also help. Check your credit reports for errors, pay off existing debt, and avoid new credit inquiries in the months leading up to your loan application[1][3][5].

Finally, don’t hesitate to walk away if the offered rate isn’t competitive. With a solid preapproval in hand, you have the flexibility to choose financing that better suits your needs.

Conclusion

Grasping the concept of APR is a game-changer when it comes to financing a vehicle. APR goes beyond just the interest rate - it factors in additional mandatory costs like origination fees, documentation charges, and other lender expenses. This gives you a clearer picture of the true annual cost of borrowing, making it easier to fairly compare options across banks, credit unions, and dealership financing offers.[1] While the interest rate alone only tells part of the story, APR ensures you see the full picture.

Even a small difference in APR can lead to significant savings over the life of your loan. That’s why focusing solely on the monthly payment can be misleading. Sometimes, a slightly higher monthly payment paired with a lower APR can save you more in the long run and help you pay off the loan faster.[1]

Factors like your credit score, debt-to-income ratio, down payment, loan term, and the vehicle’s age heavily influence the APR you’re offered.[1] Before you start shopping, take steps to improve your financial standing: check your credit, pay down existing debt, and aim for a larger down payment. Getting preapproved is another smart move - it gives you a benchmark to compare offers and strengthens your position when negotiating.

When comparing APRs, make sure you’re looking at written offers from at least two or three lenders for the same loan amount, term, and down payment. This ensures your comparisons are meaningful. Be on the lookout for red flags like vague fees, APRs that unexpectedly increase at signing, or pressure to accept add-ons like extended warranties or insurance products that drive up costs without clear benefits. Always review the Truth in Lending disclosure to confirm that the APR, finance charge, and total payments match what was promised.

If a deal doesn’t feel right, don’t hesitate to walk away. Some dealerships and lenders, like Hello Motors, offer flexible options for a range of credit profiles, but it’s still essential to compare APRs and terms just as you would with a traditional bank or credit union. Even if dealership financing seems convenient, protect yourself by carefully reading every disclosure, asking about all fees, and ensuring the loan aligns with your long-term budget.

To make a smart decision, verify your credit, set a realistic budget, get preapproved, and compare written APR offers. Scrutinize every financing document and prioritize long-term affordability over a slightly lower monthly payment. By understanding how APR works and the factors that influence it, you’ll be better prepared to secure financing that saves you money and supports your financial goals for years to come.