Inflation has pushed up used-car prices and auto loan APRs, raising monthly payments and total interest—hit hardest for buyers with lower credit scores.

Published Date:

25 févr. 2026

Last Updated:

25 févr. 2026

How Inflation Impacts Auto Financing for Used Cars

Inflation is driving up the cost of buying used cars by increasing both vehicle prices and auto loan interest rates. Here's what you need to know:

Rising Interest Rates: As of February 2026, the federal funds rate is 3.5%–3.75%, leading to higher auto loan APRs. Average rates for used car loans reached 11.54% in mid-2025.

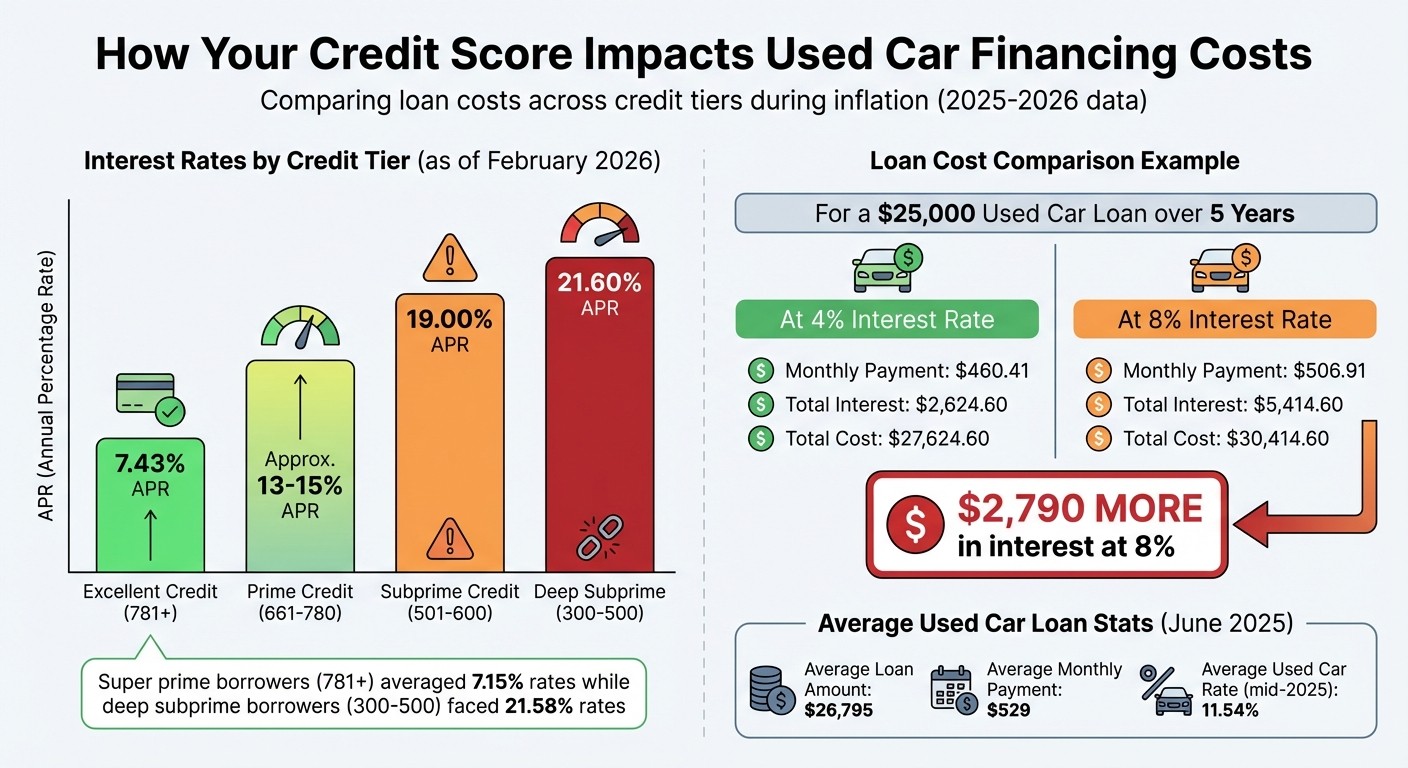

Higher Vehicle Prices: Inflation has also pushed up the cost of used cars. By June 2025, the average loan amount for a used vehicle was $26,795, with monthly payments averaging $529.

Impact by Credit Score: Borrowers with excellent credit (781+) enjoy lower rates (around 7.43%), while subprime borrowers (501–600) face rates as high as 19%.

Loan Costs: A $25,000 used car financed at 8% over 5 years costs $2,790 more in interest than at 4%. Longer loan terms can reduce monthly payments but significantly increase total interest costs.

To manage costs, consider shorter loan terms, more affordable vehicles, or flexible financing options like in-house dealership plans. Even small improvements to your credit score can lead to big savings.

How Inflation Raises Interest Rates on Auto Loans

Federal Reserve Rate Adjustments

When inflation rises, the Federal Reserve steps in by increasing the federal funds rate - the rate banks charge each other for overnight borrowing. This move is designed to slow economic growth and curb rising prices. For instance, as of December 10, 2025, the Federal Reserve set its target range at 3.50%–3.75% [6]. When the Fed raises this benchmark rate, borrowing becomes more expensive for banks, and these costs often trickle down to consumers.

Here’s how it works: banks rely on the federal funds rate to determine their prime rate, which serves as the basis for most consumer loans. Historically, the prime rate hovers about 3% above the top of the Fed’s target range [6]. When inflation drives the Fed to hike rates, auto loan APRs tend to increase as a result.

"When the Fed raises rates, borrowing costs for banks rise, and banks typically increase rates on consumer loans (including car loans)." - Caribou [6]

This chain reaction means higher borrowing costs for consumers, including those seeking auto loans.

Effects on Lenders and Borrowers

With the Fed’s rate hikes driving up borrowing costs, lenders are forced to adjust their loan rates, including those for auto loans. While lenders may not immediately pass on rate changes, prolonged inflation increases their operational costs and financial risks, pushing them to raise APRs. This helps them protect profit margins and guard against the risk of future repayments losing value [6][7].

For those looking to browse used car inventory, the impact can be especially challenging. By April 2024, average used car loan rates had soared to 11.93% due to unexpected inflation spikes [2]. Even borrowers with excellent credit can feel the pinch, as lenders raise their baseline rates across the board. Elliot Rieth, a writer at Capital One, points out:

"If your lender decides to increase their rates alongside the federal rate, it could mean they're passing their higher costs onto you, regardless of how good your credit might be" [7].

How do inflation and interest rates affect car finance?

Higher Total Costs for Used Car Loans

How Credit Score Affects Used Car Loan Rates and Costs in 2025-2026

Loan Cost Comparison Example

Rising inflation and interest rates have led to a sharp increase in the cost of financing used cars. Let’s break it down: if you finance a $25,000 used car over five years at a 4% interest rate, your monthly payment would be about $460.41, with total interest adding up to $2,624.60. Now, bump that interest rate to 8% - a situation common during inflationary periods - and your monthly payment jumps to $506.91, with total interest skyrocketing to $5,414.60. That’s an extra $2,790 in interest alone.

This steep increase has pushed many buyers to take out larger loans just to afford similar vehicles. The Consumer Financial Protection Bureau highlights this trend:

"As car prices continue to rise, loan amounts are rising, and loan lengths are growing to make those larger loans seem affordable." [1]

And it’s not just the interest rates - higher vehicle prices are adding even more pressure to consumers’ budgets.

Inflation's Effect on Vehicle Prices

On top of rising interest rates, inflation has driven up the price of used cars, further compounding costs. By June 2025, the average loan amount for a used vehicle hit $26,795, with average monthly payments reaching $529 [4]. While some buyers have tried to manage these increases by offering higher cash down payments or trading in vehicles with greater value, the overall trend is clear: people are paying more upfront and over the life of their loans.

Credit scores also play a big role in determining how much buyers pay. As of February 2026, interest rates varied significantly by credit tier:

7.43% for borrowers with excellent credit (781 or higher)

19.00% for subprime borrowers (501–600)

21.60% for deep subprime borrowers (300–500) [8]

U.S. News & World Report summarizes the challenge well:

"A high interest rate may negate those savings [of buying used] and could end up costing you more over time." [8]

With rising car prices and elevated interest rates, consumers are facing higher initial expenses and longer financial commitments, making used car purchases an increasingly expensive endeavor.

Flexible Financing Options During Inflation

Financing Plans for All Credit Situations

Inflation often prompts banks to tighten their lending criteria, leaving many buyers scrambling for alternatives. To address this, dealerships like Hello Motors have introduced tiered financing plans - Basic, Premium, and Custom - that cater to a range of credit profiles. These plans acknowledge that traditional lending models often don't work for everyone, especially as rising Federal Reserve rates have made it harder for subprime buyers to secure loans.

The statistics highlight the challenge: subprime buyers (credit scores under 620) made up 14% of new vehicle sales in 2018, but that figure dropped to just 6% by 2023 as interest rates climbed [3]. This has left many buyers with limited options. Tiered financing steps in by evaluating a borrower’s overall financial situation - not just their credit score. This approach often focuses on older, more budget-friendly vehicles (9+ model years), where over 55% of buyers manage to keep monthly payments under $400 [10]. By doing so, tiered financing creates a pathway for buyers who might otherwise be excluded.

Benefits of In-House Financing

In-house financing offers a key advantage during inflation: dealerships have the freedom to set their own lending criteria, bypassing the rigid rules of traditional banks. This flexibility allows for quicker approvals and terms that better suit borrowers' needs. For example, while the average used car loan rate hit 11.62% by late 2024 [9], in-house lenders take a more comprehensive view, considering factors beyond just credit scores.

Additionally, Finance and Insurance (F&I) managers at dealerships like Hello Motors work with a variety of lending partners, increasing the chances of approval even for buyers in tough situations [11]. These managers can also structure deals that traditional banks might reject, such as financing older vehicles often overlooked by major institutions [11]. This approach is especially crucial as inflation pushes buyers toward older, more affordable cars to keep monthly payments within reach. By offering these tailored solutions, in-house financing becomes a lifeline for many during challenging economic times.

Ways to Manage Auto Financing Costs During Inflation

Longer Loan Terms or Lower-Priced Vehicles

Inflation often pushes car buyers to make tough decisions: either extend the loan term to reduce monthly payments or choose a more affordable vehicle. Let’s break it down. Extending a loan term from five to seven years can lower monthly payments significantly. For instance, borrowing $45,000 at 7% interest over five years results in monthly payments of $891.05, with total interest costing $8,463.24. Stretching that to seven years drops the monthly payment to $679.17 - a reduction of $211.88 per month - but increases total interest by $3,587.09, bringing it to $12,050.33 [12].

Alternatively, opting for a less expensive vehicle, especially a used one, can help avoid higher interest costs altogether. In June 2025, the average used car loan was $26,795 with monthly payments of $529, compared to $41,983 and $749 for new cars [4]. That’s a monthly saving of about $220 without extending the loan term. Plus, used car prices dropped by 2.2% year-over-year in early 2024, further easing financing challenges [2]. Financial advisors suggest following the "five-year rule": if you can’t pay off a car within 60 months, it’s better to either choose a more affordable model or increase your down payment rather than stretching the loan term [12].

These strategies show how to manage costs effectively, and the next section highlights a comparison of financing options to guide your decision.

Financing Strategy Comparison

Inflation impacts everyone differently, so selecting the right financing approach depends on your financial situation. Shorter loan terms (36–48 months) help you build equity faster and reduce total interest but come with higher monthly payments. On the other hand, longer terms (72–84 months) offer lower monthly payments, easing cash flow, but lead to higher overall interest costs and a greater risk of negative equity. For those with unique credit needs, custom dealership financing - such as the flexible plans at Hello Motors - can provide tailored solutions.

Here’s a quick comparison of financing strategies to help you decide:

Strategy | Advantages | Disadvantages | When to Use |

|---|---|---|---|

Shorter Loans (36–48 months) | Lower total interest; faster equity growth | Higher monthly payments | You have a strong budget and want to own the car quickly |

Longer Terms (72–84 months) | Reduced monthly payments; better cash flow | Higher overall interest; risk of negative equity | Monthly affordability is your top priority during inflation |

Custom Dealership Financing | Flexible terms; easier approval | Terms depend on credit profile | If traditional banks reject your application or you need tailored financing |

Your credit score also plays a critical role in determining loan costs. As of June 2025, super prime borrowers (credit scores 781+) secured used car loan rates averaging 7.15%, while deep subprime borrowers (300–500) faced much steeper rates at 21.58% [4]. This difference can translate into tens of thousands of dollars in additional interest over the life of a loan [5]. To prepare, check your credit report at least 30 days before shopping to fix any errors, and submit all loan applications within a 30-day window to minimize the impact on your credit score [5].

Conclusion

Inflation has made buying a used car more challenging, with rising vehicle prices compounded by higher interest rates as the Federal Reserve works to stabilize the economy [3]. By late 2024, the average interest rate for used car loans hit 11.62%, while deep subprime borrowers faced staggering rates of up to 21.81% [9].

The disparity between credit tiers has also grown wider. For instance, super-prime borrowers enjoy rates around 7.67%, while subprime borrowers are stuck with rates averaging 19.38%. This difference can translate to thousands of extra dollars in loan costs [9]. Jonathan Smoke, Chief Economist at Cox Automotive, highlighted the impact:

Subprime buyers are increasingly squeezed out as rates climb [3].

To navigate these hurdles, buyers need to make strategic decisions about financing. Adjusting loan terms or choosing more affordable vehicles can help offset higher rates. Even a modest credit score improvement - say, 50 points - can lead to significant savings in interest over the life of a loan [13]. Additionally, flexible in-house financing options can provide personalized solutions for those with credit challenges.