Act fast if you bought a stolen car: file a police report, notify your insurer and lender, gather records, and contact the DMV to protect yourself.

Published Date:

25 févr. 2026

Last Updated:

25 févr. 2026

Steps to Take After Buying a Stolen Car

If you find out you’ve purchased a stolen car, act immediately to protect yourself legally and financially. Here’s what to do:

Contact law enforcement: File a police report to document the theft and protect yourself from liability if the car was used in a crime.

Notify your insurance company: Provide them with the police report and details about the vehicle. This is crucial for processing claims.

Inform your lender: If the car is financed, let your lender know about the situation. You may still need to make payments while the investigation is ongoing.

Gather purchase records: Keep all documents, including the bill of sale, receipts, and communication with the seller, to prove you bought the car in good faith.

Reach out to the DMV: Report the issue to freeze the title and prevent the car from being re-registered fraudulently.

Understanding your legal rights is important. Sellers must guarantee valid ownership, and consumer protection laws can help you recover losses. If the car is seized, you may lose both the vehicle and the money you paid, but compensation programs or legal action could offer some recourse. To avoid this in the future, always verify the VIN, check the vehicle’s history, and buy from reputable dealerships.

Key takeaway: Act fast, document everything, and seek legal or financial assistance to minimize losses.

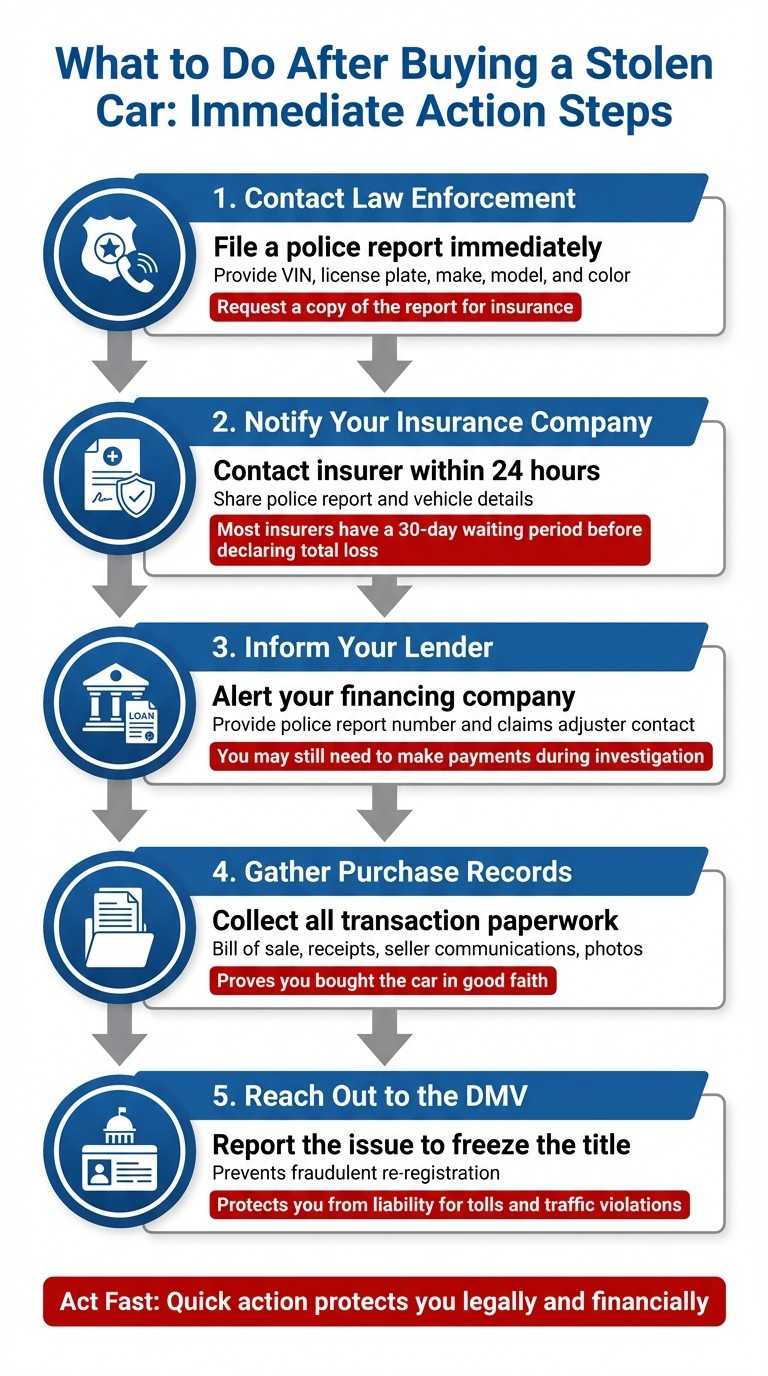

5 Immediate Steps to Take After Buying a Stolen Car

What to Do Right Away

Contact Law Enforcement

Get in touch with your local police department through their non-emergency line as soon as possible. Be ready to provide key details about your vehicle, such as the VIN, license plate number, make, model, color, and any unique identifiers. If you don’t have this information handy, check your purchase contract, insurance card, or title paperwork for reference, or browse our inventory if you need to replace your vehicle.

Filing a police report is crucial - it creates an official record that can protect you if the vehicle is used in illegal activities. Be sure to request a copy of the report (physical or digital), as your insurance company will need it when handling your claim. If you have any security footage or other evidence related to the situation, share it with the police immediately. Once this step is done, notify your insurance company to safeguard your financial interests.

Notify Your Insurance Company

Reach out to your insurance provider within 24 hours of filing the police report. Share the same detailed information about your vehicle. If your car is financed, your insurer will coordinate with your lender directly. Keep in mind that most insurance companies enforce a 30-day waiting period before officially declaring a stolen vehicle as a total loss.

In addition to informing the necessary parties, it’s important to keep all your purchase-related documents in order.

Keep All Purchase Records

Store all transaction-related paperwork - like the bill of sale, payment receipts, seller communications, and any photos of the vehicle - in a safe place away from the car itself. These documents, especially those containing the VIN, will support your claim of a legitimate purchase and help both law enforcement and your insurance company during their investigations. Also, notify the DMV promptly to prevent the vehicle from being fraudulently re-registered and to protect yourself from liability for tolls or traffic infractions tied to the car.

What Happens If You Buy a Stolen Vehicle Without Knowing?

Your Legal Rights and Options

Once you've taken immediate steps to address the situation, it's essential to understand your legal rights and the options available to recover losses and hold the responsible parties accountable.

Warranty of Title and Dealer Obligations

When you buy a vehicle, the seller is legally required to guarantee valid ownership and a marketable title, even if no written warranty is provided. If your purchase was through a dealership, they are obligated to ensure the vehicle is free of liens or other claims - no one else should have a legal stake in it [10]. For instance, in states like Texas, dealerships must register and title the car in your name within 30 days, regardless of any outstanding financing [6].

Dealers are also required to display a federally mandated Buyers Guide on used vehicles. This guide becomes part of your sales contract upon purchase. If the guide includes a warranty but your contract states "as is", the warranty in the Buyers Guide takes precedence, and the dealer must honor its terms [6][7]. Be sure to review your purchase records for this document, as it can override conflicting terms in the dealer's contract.

Consumer Protection Laws

Federal laws provide strong safeguards for buyers who unknowingly purchase stolen vehicles. The Magnuson-Moss Warranty Act allows you to take legal action if a seller breaches express warranties, implied warranties, or service contracts. According to the Federal Trade Commission (FTC), "If successful, you can recover reasonable attorneys' fees and court costs" [5]. This means you won't be burdened with legal expenses if you win your case.

In most cases, used cars come with a "warranty of merchantability." This is an implied promise that the car will function as expected, unless it was explicitly sold "as is" [5][7]. Depending on your state, this implied warranty can last up to four years [5]. If a dealer refuses to resolve a title issue, you can escalate the matter by contacting your state attorney general’s office or filing a claim in small claims court for minor disputes [5][7].

These protections emphasize the importance of documenting all steps you take, as thorough records will support your claim of a good-faith purchase.

Proving You Bought in Good Faith

To avoid criminal charges, you must prove that you were unaware the vehicle was stolen. Federal law (18 USC 2313) specifies that criminal penalties only apply if you knowingly purchased a stolen vehicle. The statute states: "Whoever receives, possesses, conceals, stores, barters, sells, or disposes of any motor vehicle... which has crossed a State or United States boundary after being stolen, knowing the same to have been stolen, shall be fined under this title or imprisoned not more than 10 years, or both" [8].

Your purchase records are your strongest evidence of good faith. Keep receipts, VIN verification documents, vehicle history reports, and any written communication with the seller. If you had the car inspected by an independent mechanic or verified the VIN through the National Insurance Crime Bureau's VINCheck service before buying, these records further solidify your case [9][5]. Such documentation demonstrates that you took reasonable steps to confirm the vehicle's legitimacy and had no reason to suspect it was stolen.

Financial Impact and Next Steps

Now that your legal rights are clearer, it’s time to address the financial fallout of discovering you’ve purchased a stolen vehicle. The financial hit can go beyond just losing the car. If law enforcement seizes the vehicle to return it to its rightful owner, you could be left without transportation and out thousands of dollars that may be unrecoverable. For instance, during the 2022–2023 fiscal year, Ontario's Motor Vehicle Dealers Compensation Fund paid out $842,000 to 128 claimants who suffered losses due to vehicle fraud and seizures [3]. While this example is specific to Canada, it highlights how this issue affects people across North America.

What Happens If the Car Is Seized

When authorities take the vehicle, it’s typically returned to its rightful owner or a creditor, leaving you without the car or any value from it. Acting quickly on the financial front is just as important as taking legal steps to minimize your losses. If you bought the car from an unlicensed seller or a "curbsider", recovering your money is almost impossible since these sellers often disappear after the sale. However, if you purchased from a licensed dealer, you might have access to state compensation funds, though these programs vary by location [3].

Getting Your Money Back

The sooner you act, the better your chances of recovering some of your money, often with the help of legal counsel. If you financed the car, contact your lender immediately and share the police report and insurance claim information so they can work with adjusters [1]. Also, confirm whether the dealer was licensed through your state’s regulatory body. Licensed dealers may offer access to compensation programs. Karen Axelton, a Senior Personal Finance Writer at Experian, explains:

If your insurance settlement is less than the loan balance, you'll be responsible for making up the remainder unless you have gap insurance to pay the difference [1].

For example, if your loan balance is $18,000 but your insurance only pays $15,000, you’d still owe $3,000. Consulting an attorney can help you explore civil claims against the seller or determine if any warranty of title protections apply. If you’re expecting a refund, it’s essential to clarify your obligations with your lender as soon as possible.

Dealing with Your Lender

Your lender will play a key role during this process. Even if the car is seized, you’re still required to make payments on the loan until your insurance claim is resolved. Provide your lender with the police report number and your claims adjuster’s contact details promptly [4]. Moses Mwangi from myAutoloan emphasizes the importance of this:

Failure to report the theft to the financing company might lead to penalties or breach of contract, potentially affecting your financial status [11].

This underscores the need to address any gaps in your insurance or legal protections. If your finance agreement includes gap insurance, it can cover the difference between your remaining loan balance and the insurance payout. If the insurance settlement exceeds what you owe, your lender will typically send you the excess amount. If there’s a shortfall and you don’t have gap insurance, ask your lender if the remaining balance can be rolled into a new auto loan [4].

How to Avoid This Problem in the Future

Preventing fraud when buying a car is all about being thorough. In 2024, over 850,000 vehicles were reported stolen across the country[14][15]. Shockingly, at least 25% of these stolen cars are resold to unsuspecting buyers[12]. By following these steps, you can protect yourself from falling into the same trap.

Check the Vehicle History

Before you buy, always verify the 17-character VIN (Vehicle Identification Number). Check it in multiple spots: the dashboard near the driver’s side windshield, the driver’s side doorframe, and the engine firewall. If the VINs don’t match or show signs of tampering like scorch marks or soldering, consider it a red flag[12][15].

Use tools like the National Insurance Crime Bureau’s VINCheck to see if the car has been reported stolen or has a salvage record[12][14]. For a deeper dive, run a title search through the National Motor Vehicle Title Information System (NMVTIS). This will reveal the car’s title history, odometer readings, and any “brands” (like junk, salvage, or flood status)[13][14]. As NMVTIS states, "A 'clean' NMVTIS report is a GOOD thing!"[13].

You can also get a vehicle history report from services like Carfax or AutoCheck to check past ownership and accident records[14][15]. Lastly, reach out to your insurance company - they may have access to theft flags not yet listed in public databases[14][15].

Buy from Reputable Dealerships

Choosing the right dealership is one of the best ways to avoid buying a stolen or cloned car. Trusted dealerships are less likely to sell vehicles with fraudulent VINs or questionable histories[15]. They typically provide clear titles, maintenance records, and the previous bill of sale[15]. To be extra cautious, have a professional mechanic inspect the car for any signs of tampered VIN plates or hidden damage[15].

Always check the dealership’s reputation. You can verify their legitimacy through the Federal Trade Commission (FTC) or your state attorney general’s office[16]. Renee Valdes, Lead Editor at Kelley Blue Book, offers wise advice: "If the price is too good to be true, or the seller is overly eager to sell you the car and is urging you to skip steps in the car-buying process, trust your instincts."[15] Be prepared to walk away if the seller refuses to provide proper identification, insists on email-only communication, or demands a deposit before you’ve even seen the car[14].

Review All Sales Documents Carefully

Once you’ve found a vehicle, examine the paperwork with a fine-tooth comb. Ensure the VIN is consistent across the title, registration, insurance documents, and the car itself[14]. Look for official state seals or watermarks on the title - these confirm it’s authentic[14].

The name on the title should match the seller’s government-issued ID. Ask to see the original bill of sale to verify the chain of ownership[14][15]. Also, cross-check dates and mileage on the maintenance records with third-party vehicle history reports for consistency[15]. In some states, like Florida, New York, and Georgia, a “salvage” title is used to mark vehicles that were once stolen[14]. Keep an eye out for that designation to avoid surprises later.

Conclusion

The steps outlined above offer a straightforward way to protect both your rights and your finances. Realizing you've unknowingly purchased a stolen car can be overwhelming, but acting quickly and responsibly is key to minimizing the fallout. Start by reaching out to law enforcement to file a police report - this is a critical first step. It not only supports your insurance claim but also shows you acted in good faith. As attorney Clayton Hasbrook points out:

Comprehensive insurance does cover incidents that aren't under one's control, such as theft. [4]

After involving the police, notify your insurance provider, the Department of Motor Vehicles (DMV), and your lender if the car is financed. These steps help secure the vehicle's title, protect you from further liability, and initiate the process of recovering your financial losses.

Keep in mind, even if the car is repossessed, you might still need to continue making loan payments until your insurance claim is resolved. GAP insurance can help by covering the difference between what you owe on the loan and the car’s actual cash value. [1][2] To strengthen your case, maintain all purchase records, contracts, and any communication with the seller. These documents are essential for proving you acted in good faith and for pursuing legal action if necessary.