Used car prices in Ontario remain high because fewer new cars, chip shortages and higher loan rates have tightened supply; experts expect relief after 2028.

Published Date:

17 janv. 2026

Last Updated:

17 janv. 2026

Why Used Car Prices Stay High in Ontario

Used car prices in Ontario remain high due to a mix of limited supply and increased demand. Key factors include:

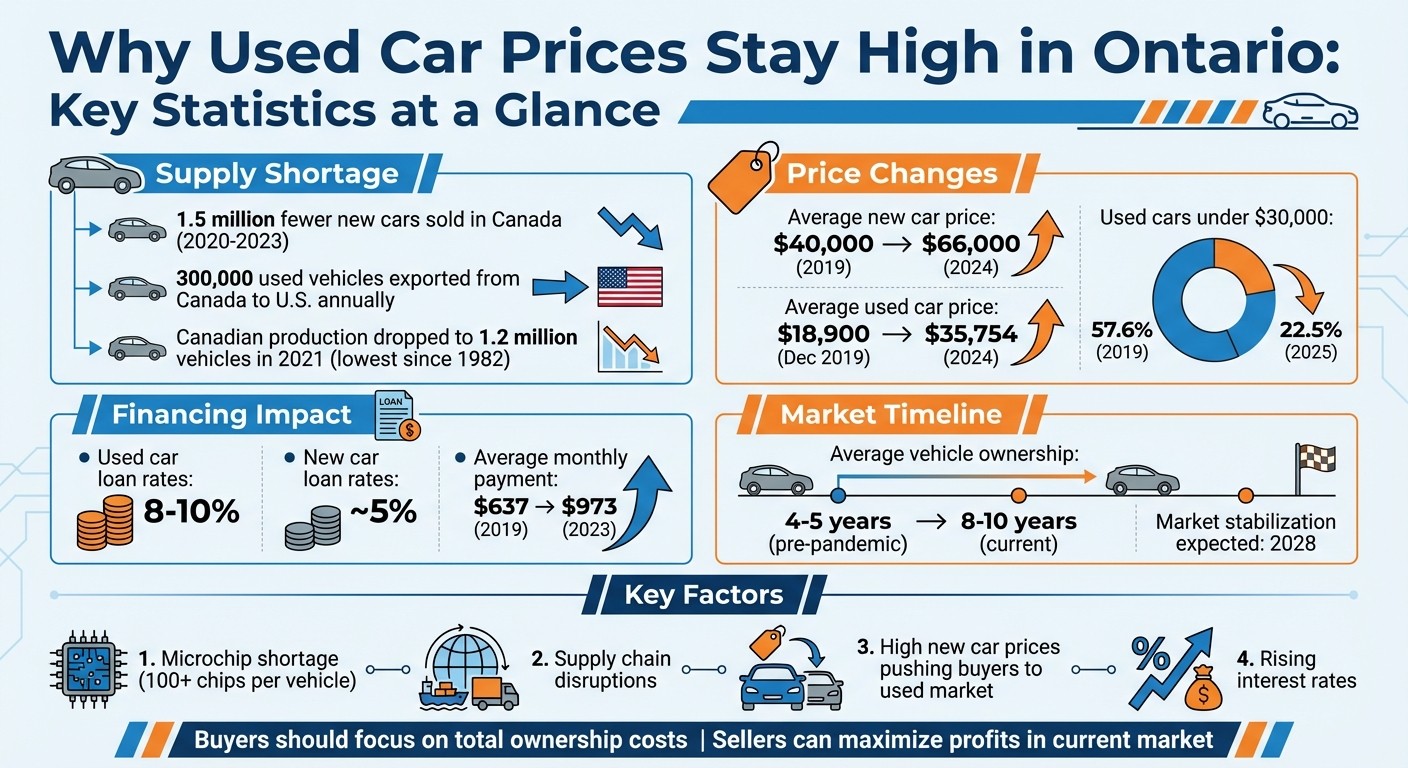

Fewer New Cars Sold (2020–2023): Canada sold 1.5 million fewer new cars during this period, reducing trade-ins and lease returns.

High New Car Prices: The average price of a new car rose from $40,000 in 2019 to $66,000 by 2024, pushing buyers to browse used vehicle inventory.

Supply Chain Issues: The global microchip shortage and pandemic-related disruptions significantly slowed vehicle production.

Rising Financing Costs: Loan rates for used cars now range from 8–10%, increasing monthly payments.

The result? A tighter inventory and higher prices. Experts predict the market won’t stabilize until at least 2028. Buyers should focus on total ownership costs, while sellers can take advantage of the strong demand to maximize profits.

Ontario Used Car Market Statistics: Price Increases and Supply Shortage 2019-2024

Used car sales in Canada rev up as prices continue to climb across the board

How Global Supply Chain Problems Continue to Affect Prices

The pandemic sparked a chain reaction that continues to ripple through Ontario's used car market. Back in early 2020, when COVID-19 hit, automakers slashed their semiconductor orders, anticipating a sharp drop in demand. But demand bounced back faster than expected, and chip manufacturers had already shifted their focus to consumer electronics. The result? A massive shortfall of 18 million vehicles globally. In Canada, production plummeted to just 1.2 million vehicles in 2021 - the lowest annual total since 1982. Ontario, home to major car manufacturing plants, felt the brunt of this crisis. In October 2021, Stellantis laid off 1,800 workers at its Windsor assembly plant and cut an entire production shift, while GM's CAMI facility in Ingersoll sat idle for most of the year [8]. This production gap set off a domino effect, reshaping the microchip market and disrupting vehicle manufacturing on a large scale.

The Microchip Shortage and Its Impact

Today’s vehicles are heavily reliant on microchips, with each car requiring over 100 custom chips. Electric vehicles (EVs) take this to another level, needing up to eight times as many [1][9]. Dr. Peter Frise, Director of the Centre for Automotive Research & Education at the University of Windsor, explains:

"The average new vehicle has upwards of 100 chips, and many have lots more... they are not interchangeable. Each type is custom-designed for its application." [9]

This shortage didn’t just slow down production lines - it also reshaped consumer behavior. With new cars stuck on lengthy waitlists, many buyers turned to the used car market. The result? Prices soared. In some cases, 2-3-year-old vehicles sold for more than their original sticker price [7]. Rob Fekhon, Sales Manager at Anew Auto Sales, highlights the competitive pressure:

"There's multiple dealers trying to buy the same vehicles, so prices have skyrocketed. You kind of have to stay competitive and try to offer as much as you can and that's jacking up the prices." [7]

Manufacturing Delays Caused by the Pandemic

The microchip shortage wasn’t the only issue. The pandemic caused a domino effect of supply chain disruptions. Ports became clogged, railyards overflowed, and warehouses ran out of space. Bob Armstrong, former President of the Association of International Automobile Manufacturers, paints a vivid picture:

"The supply chain backed up worldwide and then what happened is our ports got full ... the railyards were full, every warehouse in the country was full." [1]

This production gap has created a long-term inventory problem. New cars typically re-enter the market as off-lease vehicles after about four years, but those cars simply aren’t there because they were never sold in the first place. Daniel Ross, Senior Manager of Auto Industry Insights at Canadian Black Book, puts it bluntly:

"Those vehicles are not coming back to the market because they were not sold new." [2]

Adding to the problem, rental companies - normally a key source of 1-3-year-old used vehicles - sold off their fleets early in the pandemic. Now, they’re struggling to restock [7].

Pricing Trends Across Canada

Ontario, as Canada’s automotive manufacturing hub, has felt these challenges more intensely than most provinces. When plants in Windsor, Oakville, and Ingersoll halt production, the impact on local supply is immediate. The numbers tell the story:

Metric | Pre-Pandemic (2019) | Post-Shortage (2024) |

|---|---|---|

Annual Canadian New Sales | 2.0 Million | 1.5 – 1.6 Million |

Average Monthly New Payment | $637 | $973 |

Experts believe these supply chain issues won’t fully resolve until at least 2028 [2]. For Ontario residents, the scarcity is palpable. Take Mohammed Merchant from Ajax, Ontario, for example. In July 2021, he had to search the entire Greater Toronto Area and drive 62 miles just to find a 2014 Toyota Prius - a direct consequence of the production halt [10]. This kind of scarcity has become the norm, not just in Ontario but across Canada. As global challenges persist, both buyers and sellers in Ontario are being forced to rethink their strategies in this tight market.

What's Keeping Used Car Prices High in Ontario

Expensive New Cars and Low Used Car Supply

Ontario’s used car market is feeling the effects of what some call the "missing million" vehicles. Between 2020 and 2023, Canada sold about 1.5 million fewer new cars than usual [2][3]. This shortfall has left a noticeable gap in trade-ins and lease returns, which are key sources of used car inventory.

On top of that, new car prices have soared, with the average price jumping from $40,000 in 2019 to a staggering $66,000 [2]. As a result, many buyers are turning to used cars. But here’s the catch: the supply of affordable used cars has plummeted. Back in 2019, 57.6% of used cars were priced below $30,000. By mid-2025, that number had dropped sharply to just 22.5% [13]. Baris Akyurek, Vice President of Insights and Analysis at Auto Trader, summarizes the issue:

"As it is, the used car market is constrained... 1.5 million fewer car sales translates into fewer new cars and trade-ins hitting the market" [3].

The problem is compounded by lease holders choosing to keep their vehicles instead of returning them. Leased cars make up about 35% of the market [2], but with replacement costs so high, many drivers are opting to hold on to their cars. Rental companies, another major source of nearly-new vehicles, are also holding onto their fleets longer because they can’t secure enough new cars [7]. To make matters worse, around 300,000 used vehicles are exported from Canada to the U.S. every year [7], further tightening supply in Ontario. This lack of inventory not only limits options for buyers but also keeps prices stubbornly high.

How Interest Rates and Inflation Affect Prices

Financial pressures are adding fuel to the fire. Loan rates for used cars are currently between 8% and 10%, compared to roughly 5% for new vehicles [2]. Combined with inflated car prices, this has pushed average monthly payments from $637 in 2019 to $973 by 2023 [2].

Inflation is another factor keeping costs high. Rising prices for gas, parts, and labor make car ownership more expensive overall. Many people are holding onto their vehicles longer to avoid the steep costs of replacing them or financing a new purchase [12][13]. In fact, the average age of trade-in vehicles rose from 7.3 years to 7.6 years in just one year [4].

This creates a tricky situation. Normally, high costs would reduce demand, but with supply so limited, prices remain elevated [12][13]. Even though the Bank of Canada lowered its benchmark rate to 2.25% in October 2025 [14], used car loan rates haven’t dropped significantly, keeping financing costs high for Ontario buyers.

Ontario's Market Characteristics

Ontario faces additional challenges that intensify these issues. As Canada’s automotive manufacturing hub, production delays at plants in Windsor, Oakville, and Ingersoll have directly impacted local inventory. These disruptions add to the supply crunch already affecting the market.

The province’s large population and urban-suburban sprawl ensure steady demand for vehicles. The pandemic accelerated a shift toward suburban living, making car ownership essential for many who previously relied on public transit [7]. This trend hasn’t reversed, keeping demand strong even as prices climb. In early 2025, used car sales were up 15.7% year-over-year, with many vehicles selling quickly after being listed [3].

Ontario’s regulatory environment also adds complexity. The Ontario Motor Vehicle Industry Council (OMVIC) allows dealers to advertise two prices: one for cash and a discounted price for financing, as long as both are clearly displayed [3]. While this practice is legal, it can make comparison shopping more difficult. Often, the lowest advertised price comes with high-interest loans, making it harder for buyers to gauge the true cost. Adding to the pressure, recent U.S. tariffs have pushed about 30% of surveyed buyers to switch from new cars to used ones [3], further increasing competition for already limited inventory.

How Ontario Buyers and Sellers Can Handle High Prices

Tips for Buyers: Getting the Best Deal

Navigating Ontario's competitive market requires smart strategies and a flexible mindset. Take Erika Weber, for example - she managed to cut her budget nearly in half in March 2022 by widening her search area and considering a flipped car. Her story highlights how creative thinking can lead to big savings [11].

Another key tip? Focus on the total cost of ownership. Shari Prymak, Executive Director of Car Help Canada, advises that a used car should cost 20% to 30% less than its new counterpart to offset higher interest rates.

"If you're not saving at least that amount of money, then buying a used car doesn't make sense" [5].

Crunching the numbers is essential in today’s market.

Consider lease buyouts, check the Used Vehicle Information Package (UVIP) for liens, and always have a trusted mechanic inspect the car before buying. Financial planner Cindy Marques emphasizes:

"It's not a matter of waiting for interest rates to go down but to bite the bullet and buy different cars than they hope they would get" [6].

If you're eyeing a car that's 20 years or older - or paying less than the Canadian Red Book value - get a professional appraisal. This step can help you reduce the 13% Retail Sales Tax [15].

For financing, platforms like Hello Motors offer flexible options such as personalized payment plans and home delivery, making it easier to handle high prices. When comparing financing deals, pay attention to the Annual Percentage Rate (APR) instead of just monthly payments. Submitting all your loan applications within a 14- to 45-day period can also help minimize the impact on your credit score [17].

Tips for Sellers: Getting Top Dollar for Your Vehicle

If you're selling, there are plenty of ways to maximize your profit. Start by setting a competitive price using tools like the CARFAX Canada Value Range. Including a detailed Vehicle History Report is crucial, as 81% of online shoppers will skip listings without one [16]. Service records, extras like winter tires, and recent replacements (e.g., brakes or batteries) can further justify a higher asking price in Ontario's tight market [16].

Professional detailing can also boost your car’s perceived value. A spotless interior, odor-free cabin, and high-quality photos taken in good lighting can make your online listing stand out. With 63% of Canadian car shoppers doing their research online - and 42% starting on listing sites [16] - a polished presentation is a must.

In Ontario, you’ll need to provide a UVIP and a signed Bill of Sale [15]. Double-check that the Vehicle Identification Number (VIN) matches your green ownership permit before listing. When it comes to payments, accept only cash or bank drafts in person to avoid fraud. Steer clear of personal checks or wire transfers [16]. Also, remember to remove your license plates and keep the "plate portion" of the ownership permit; plates don’t stay with the vehicle [15].

Selling privately often brings in more money than trading in at a dealership, though it does require extra effort and careful marketing [16].

Comparison Tables to Help You Decide

Here’s a side-by-side look at your options to help you make an informed decision:

Option | Upfront Cost | Monthly Payment | Best For |

|---|---|---|---|

Keep Current Vehicle | Maintenance only | None (if paid off) | Owners of reliable, paid-off cars |

Buy Used (2–3 years old) | ~$35,754 [5] | Higher due to 8–10% financing rates | Buyers seeking reliability without new car pricing |

Buy New | ~$66,000 [5] | Lower rate (~5%) but higher total | Those who can afford premium pricing and want the latest features |

Lease Buyout | Predetermined price | Depends on financing | Current lessees with favorable buyout terms |

When deciding based on a vehicle’s age, consider both the sticker price and long-term ownership costs:

Vehicle Age | Price Range | Financing Rate | Key Consideration |

|---|---|---|---|

1–3 years old | $30,000–$45,000 | 8–10% | Low mileage and warranty coverage |

4–7 years old | $20,000–$30,000 | 8–10% | A balance of value and reliability |

8–10 years old | $10,000–$20,000 | 8–10% to 10%+ | Maintenance costs may start to increase |

20+ years old | Under $10,000 | 10%+ or cash only | Requires appraisal for tax savings and a repair budget |

Your decision should align with your financial situation, how long you plan to keep the car, and your comfort level with potential maintenance costs. With Ontarians now holding onto their vehicles for 8 to 10 years - double the pre-pandemic average of 4 to 5 years [6] - choosing a car built to last is more important than ever.

Conclusion: Dealing with High Used Car Prices in Ontario

Ontario’s used car market has undergone a dramatic shift, and there’s no sign of it returning to pre-pandemic pricing anytime soon. A vehicle shortage - estimated at one million units between 2020 and 2023 - has created a supply crunch that experts predict will last until at least 2028 [2][5]. With average used car prices now sitting at $35,754, nearly double the $18,900 average from December 2019, both buyers and sellers must adjust their expectations to reflect this new reality.

For buyers, understanding the true cost of ownership is essential. The general rule of thumb is that a used car should cost at least 20% to 30% less than its new equivalent. If not, the higher interest rates typically associated with used car loans can cancel out any perceived savings. Instead of focusing solely on the sticker price, consider factors like financing costs, maintenance, insurance, and fuel expenses [2][5].

Sellers, on the other hand, are in a strong position to benefit from the current market. With dealerships actively seeking quality used cars - especially three-year-old models - trade-in values are higher than usual [4]. If your vehicle is well-maintained, this could be the perfect time to sell or trade it in, taking advantage of the limited supply and high demand.

For a smoother experience, working with established local dealerships like Hello Motors can be a game-changer. They offer flexible financing options tailored to various credit situations, personalized payment plans, and even home delivery. Their multilingual support team and partnerships with financial lenders provide additional resources, especially for those navigating high-interest rates.

As the market continues to evolve, both buyers and sellers need to stay sharp. Whether you’re purchasing or selling, focus on the numbers, explore your options, and don’t hesitate to seek professional advice when needed. Strategic decisions now can make all the difference in Ontario’s challenging car market.