Compare leasing and financing in Ontario: monthly costs, ownership, mileage limits, taxes, insurance and long-term costs to choose what fits your driving needs.

Published Date:

Feb 9, 2026

Last Updated:

Feb 9, 2026

Leasing vs Financing: Pros and Cons for Ontario Drivers

When deciding whether to lease or finance a car in Ontario, your choice depends on your budget, driving habits, and long-term goals. Here's a quick breakdown:

Leasing: Lower monthly payments (30%-60% less than financing), access to new cars every few years, and predictable costs under warranty. However, it comes with mileage limits, wear-and-tear fees, and no ownership equity.

Financing: Higher monthly payments, but you own the car outright after the loan is paid off. No mileage limits, freedom to customize, and potential long-term savings. Be mindful of depreciation, maintenance costs, and negative equity risks.

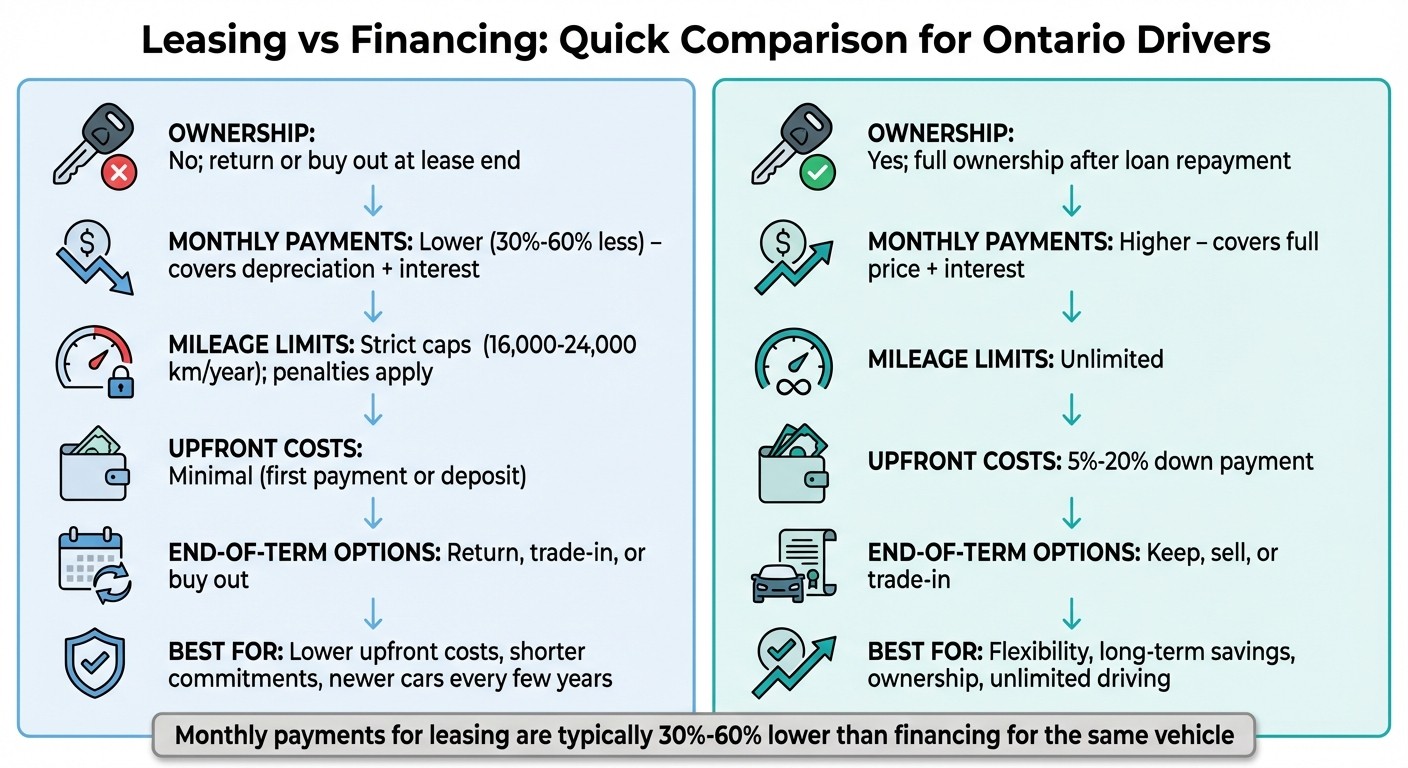

Quick Comparison:

Factor | Leasing | Financing |

|---|---|---|

Ownership | No; return or buy out at lease end | Yes; full ownership after loan repayment |

Monthly Payments | Lower (covers depreciation + interest) | Higher (covers full price + interest) |

Mileage Limits | Strict caps (16,000–24,000 km/year); penalties | Unlimited |

Upfront Costs | Minimal (first payment or deposit) | 5%-20% down payment |

End-of-Term Options | Return, trade-in, or buy out | Keep, sell, or trade-in |

If you value flexibility, long-term savings, and ownership, financing may suit you better. If you prefer lower upfront costs, shorter commitments, and newer cars, leasing could be the way to go. Consider your driving needs and financial situation before making a decision.

Leasing vs Financing Comparison for Ontario Drivers

Pros and Cons of Leasing in Ontario

Benefits of Leasing

Leasing comes with several perks, starting with lower monthly payments. These payments are generally 30% to 60% less than what you'd pay if you financed the same vehicle over the same term [4]. This is because you're essentially covering the car's depreciation during the lease period, rather than its full purchase price.

Another plus is warranty coverage. Most leases last between 2 to 4 years, which often aligns perfectly with the manufacturer's warranty period [2][7]. This can help keep your repair costs predictable and low.

Leasing also gives you access to newer technology. It allows you to upgrade to a vehicle with the latest safety and performance features every few years [8][5].

There's also a tax advantage in Ontario. Instead of paying HST on the entire value of the car, you only pay it on your monthly lease payments [8][5]. Additionally, with a closed-end lease, you avoid the risk of negative equity since you can simply return the vehicle at the end of the lease term, provided it's in good condition [2][7].

While these benefits make leasing appealing, it's important to weigh them against the potential downsides.

Drawbacks of Leasing

Leasing isn't without its limitations, and some of these can affect your long-term financial plans.

One common drawback is mileage caps. Lease agreements typically limit annual mileage to 16,000–24,000 km [8][5]. If you exceed these limits, you'll face extra charges. If you anticipate driving more, it's worth negotiating a higher mileage allowance at the start.

Another issue is wear and tear penalties. Damage like windshield cracks, upholstery stains, or worn tires can lead to additional fees at the end of your lease [2]. To avoid surprises, consider having a dealer provide an estimate of repair costs before your lease-end inspection.

Leasing also means no equity buildup. Unlike financing, where you eventually own the car, leasing leaves you with no ownership stake. Ending or renegotiating a lease early can also result in steep penalties [2]. At the end of the lease, your options are limited to starting a new lease or paying the buyout price.

Additionally, leasing comes with stricter insurance requirements in Ontario. You'll need to add specific endorsements (OPCF 5 and OPCF 43), along with collision and comprehensive coverage [5].

Leasing Pros and Cons Summary

Advantages | Disadvantages |

|---|---|

Monthly payments 30%–60% lower than financing [4] | No equity or ownership buildup |

Wear and tear penalties at lease end [2] | |

More stringent insurance requirements [5] | |

Early termination penalties | |

Restrictions on modifications and customization [3] |

Pros and Cons of Financing in Ontario

Benefits of Financing

Financing a vehicle comes with some clear perks, especially when compared to leasing. One of the biggest advantages is building equity. Once you make that final payment, the car is yours - no strings attached. You can keep driving it for as long as you like, sell it whenever you want, or even trade it in and use the equity toward your next vehicle purchase [10][4].

Another major plus? No mileage limits. Unlike leasing, which often comes with strict mileage caps and costly overage fees, financing gives you the freedom to drive as much as you need. Plus, you can personalize your car however you see fit. Whether you're adding performance upgrades, custom paint jobs, or interior tweaks, the choices are entirely up to you [10][4].

Although the monthly payments for financing are higher than leasing, there’s a long-term financial upside. Once your loan term - usually between 12 and 96 months - ends, you’re done with monthly payments. And in Canada, most car loans don’t penalize you for paying them off early, which can save you money on interest [9][11].

In Ontario, there’s also a tax advantage when trading in a financed vehicle. You only pay the 13% HST on the price difference between the new car and your trade-in value, instead of being taxed on the full price of the new vehicle. This can lead to some decent savings at the dealership [13].

Drawbacks of Financing

Of course, financing isn’t without its downsides. The most noticeable drawback? Higher monthly payments. These payments are typically 30% to 60% more than lease payments for the same vehicle, as you’re paying off the full purchase price plus interest [7][12].

Another issue is maintenance costs. Once the manufacturer’s warranty expires, any repairs come out of your pocket. And if your financing term is longer than the warranty - say, a seven-year loan with a five-year warranty - you could end up stuck paying for repairs while still making monthly payments. Automotive journalist Stephanie Wallcraft puts it plainly:

If the terms of your warranty don't align with your financing term - e.g., you have a five-year new vehicle warranty but seven-year financing - you're stuck paying for that vehicle even if it starts giving you trouble once it's out of warranty [3].

There’s also the risk of negative equity. Long loan terms (like 72 or 84 months) or small down payments can leave you owing more on the car than it’s worth. Cars depreciate quickly - most lose about 25% of their value in the first year [14]. If you need to sell or trade in early, you could end up "upside down" on your loan.

Lastly, lenders in Ontario typically require collision and comprehensive insurance throughout the loan term, which costs more than basic liability coverage [5][12].

These factors highlight the trade-offs of financing, especially when compared to leasing.

Financing Pros and Cons Summary

Advantages | Disadvantages |

|---|---|

Full ownership and equity building | Higher monthly payments |

No mileage restrictions | Responsible for maintenance after the warranty expires |

Freedom to customize and modify | Risk of negative equity with long loan terms |

Payment-free period after the loan ends | Warranty may expire before the loan term ends |

Ability to pay off your loan early (open loans) | Higher insurance requirements |

Trade-in tax savings (13% HST on the difference only) | Bears full depreciation risk |

Leasing vs. Buying: What’s Right for You?

Leasing vs Financing: Key Differences

When deciding between leasing and financing a vehicle in Ontario, understanding the main distinctions can save you from unexpected expenses. The primary difference lies in ownership. Financing allows you to eventually own the car outright after paying off the loan, while leasing is more like a long-term rental. In a lease, the dealership or manufacturer retains ownership unless you choose to buy the car at the end of the term through a buyout option [7][6].

Another key difference is the payment structure. Monthly payments for a lease are typically 30% to 60% lower than financing payments for the same vehicle, term, and price [4]. This is because leasing only covers the vehicle's depreciation during the lease period, whereas financing involves paying off the car's full purchase price plus interest. Think of leasing as paying for the use of the car, while financing is like a mortgage where you eventually gain full ownership [1].

Mileage limits are another factor to consider. Leasing comes with strict mileage caps - usually between 16,000 and 20,000 kilometers per year - with additional fees ranging from $0.08 to $0.20 per kilometer if you exceed the limit [6]. On the other hand, financing gives you the freedom to drive as much as you want without penalties.

Upfront costs also vary between the two. Leasing generally requires minimal upfront expenses, often just the first payment or a small deposit. Financing, however, typically requires a down payment of 5% to 20% of the car's price. Additionally, HST (13%) is applied differently: it's spread across monthly lease payments for leases but charged upfront for financed vehicles [15].

Side-by-Side Comparison Table

Factor | Leasing | Financing |

|---|---|---|

Ownership | No ownership; return or buy out at end of term | Full ownership once the loan is paid off |

Monthly Payments | Lower (covers depreciation + interest) | Higher (covers full price + interest) |

Mileage Limits | Strict limits (16,000–20,000 km/year); overage fees | No limits; drive as much as you want |

End-of-Term Options | Return, trade-in, or buy out at residual value | Keep, sell, or use as trade-in equity |

Upfront Costs | Minimal; often just the first payment | Typically 5–20% down payment required |

Wear and Tear | Fees for excessive damage (dents, scratches) | Owner's responsibility; impacts resale value |

HST Application | 13% applied to each monthly payment | 13% applied to the full purchase price upfront |

Customization | Typically not allowed; must return in original condition | Full freedom to modify or customize |

Early Exit | Difficult and costly; termination fees apply | More flexible; can sell or trade anytime |

Which Option is Right for You?

What to Consider Before Deciding

When deciding between leasing and financing, a few key factors can help guide your choice. Start by estimating your annual mileage. Think about your daily commutes, weekend getaways, and any long-distance trips you might take. This is especially important if you're considering a lease, as most leases come with mileage caps - usually between 10,000 and 15,000 miles per year (about 16,000 to 24,000 kilometers). Exceeding these limits can result in penalties ranging from 12 to 30 cents per mile [16]. If your driving habits suggest you'll go over these limits, financing might be the better option, as it offers unlimited mileage with no extra fees.

Your budget and financial goals are equally important. Leasing typically comes with monthly payments that are 30%–60% lower than financing [4], but it doesn't allow you to build equity. On the other hand, financing lets you build equity over time. Once you've paid off your loan, you can enjoy a period without payments and have the option to sell or trade the car. If you're planning for long-term ownership, financing tends to be more cost-effective [4].

Lifestyle and vehicle preferences also play a role. Leasing is ideal if you enjoy driving a new car every few years and want to avoid unexpected repair costs, as leases often keep you under warranty [4]. Financing, however, is better suited for those who want the freedom to customize their vehicle or plan to keep it for many years. It's worth noting that vehicle-related expenses account for nearly 20% of the average Canadian's annual income [5]. Considering these factors can help you decide whether leasing's lower payments or financing's long-term equity aligns better with your needs.

How Hello Motors Can Help

Hello Motors simplifies the decision-making process by offering flexible auto financing solutions designed for Ontario drivers, regardless of credit history. Their easy-to-use online application provides quick approvals, saving you the time and hassle of visiting multiple dealerships [17]. Plus, every on-time payment is reported to credit bureaus, which can help boost your credit score over time [17].

With financing terms available for up to 96 months, Hello Motors can help you achieve monthly payments comparable to leasing while still building ownership equity. They also deliver vehicles directly to your home and offer support in multiple languages, including English, French, Spanish, and Arabic, ensuring you get personalized advice to make the best choice between leasing and financing.

Conclusion

Choosing between leasing and financing comes down to your personal priorities and lifestyle. Leasing typically offers 30% to 60% lower monthly payments compared to financing, keeps you in a newer vehicle under warranty, and provides access to the latest features. However, it doesn't allow you to build equity and comes with mileage restrictions. On the other hand, financing requires higher monthly payments but leads to full ownership, eliminating car payments once the loan is paid off and potentially saving you money in the long run [1].

Your driving habits play a big role in this decision. If you drive more than the standard mileage limits of a lease, financing may be the better choice since it offers unlimited mileage with no penalties. But if you enjoy driving a new car every few years and can stay within mileage limits, leasing might align better with your preferences [5].

While financing helps you build equity over time, leasing means ongoing payments. However, leasing does let you enjoy the latest technology and safety features without the commitment of ownership.

Hello Motors makes this decision easier by offering flexible financing options with terms up to 96 months. Their competitive monthly payment plans help you build ownership, and their quick online approval process ensures a smooth experience. They even provide personalized guidance tailored to your financial situation and credit profile, helping you find the best fit for your needs.