2026 Canadian auto loan APRs by credit tier — ranges from 1.99% promo to 34.99% for deep subprime, plus effects of loan term, vehicle age, and down payment.

Published Date:

6 mars 2026

Last Updated:

6 mars 2026

Average Auto Loan Rates by Credit Score in Canada

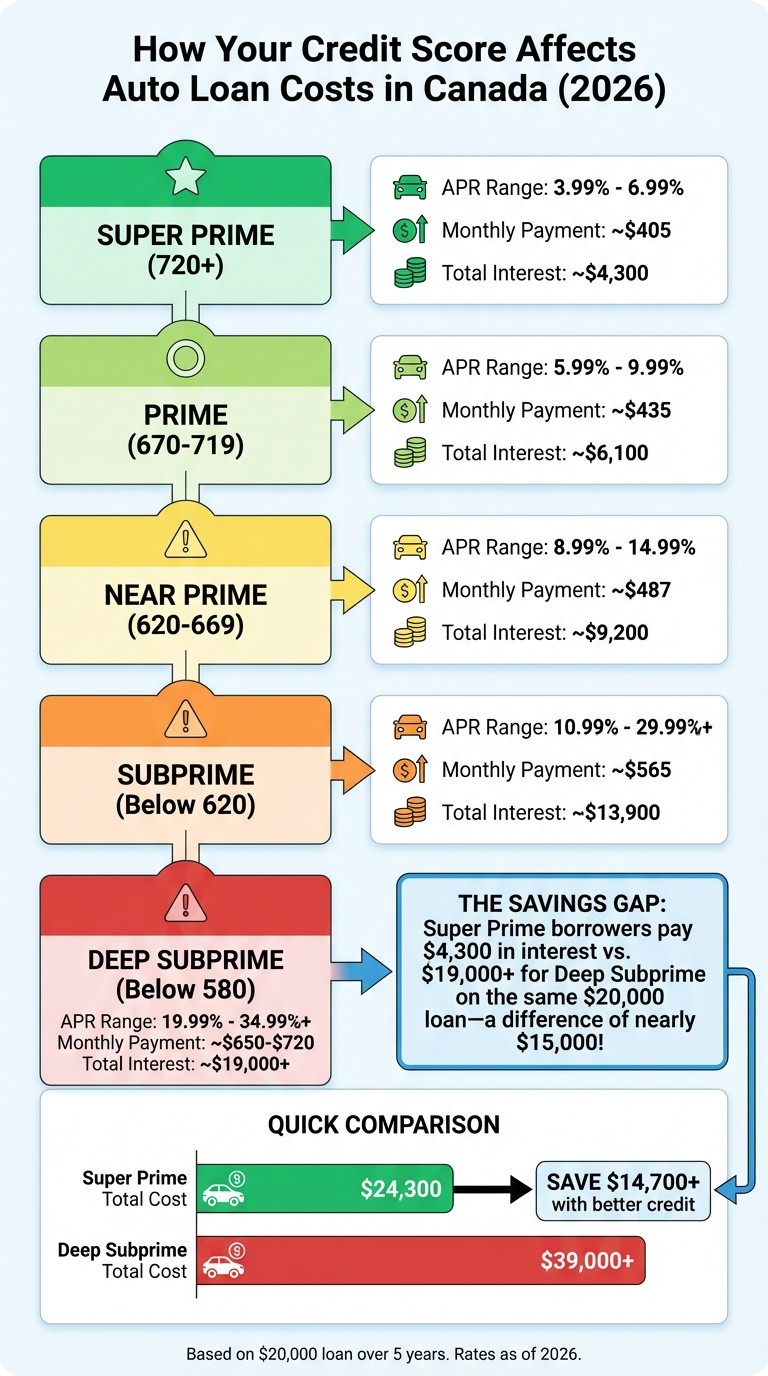

Your credit score has a direct impact on the interest rate you’ll get for an auto loan in Canada. Higher scores mean lower rates, saving you thousands over the life of a loan, while lower scores lead to higher rates and costs. As of 2026, here’s what you can expect:

Super Prime (720+): Rates from 3.99% to 6.99%.

Prime (670–719): Rates from 5.99% to 9.99%.

Near Prime (620–669): Rates from 8.99% to 14.99%.

Subprime (Below 620): Rates from 10.99% to 29.99%+.

For example, on a $20,000 loan over five years, someone with a top-tier score (760+) may pay $4,300 in interest, while a borrower with poor credit (600–639) could pay $13,900 or more. Even a small improvement in your score can lead to significant savings. Other factors, like loan term, vehicle type, and down payment, can also affect your rate.

Auto Loan Rates by Credit Score in Canada 2026

Credit Scores for Buying a Car: Current Tiered Rates & Scores (Former Dealer Explains)

Auto Loan Rates by Credit Score Range

As we move into late 2025 and early 2026, auto loan rates vary significantly based on credit score. Let’s break down what borrowers can expect in each credit tier.

Super Prime (720+): 3.99% to 6.99%

Borrowers with credit scores of 720 and above fall into the super prime category. These individuals, known for their strong credit history and consistent on-time payments, represent the lowest risk to lenders. As a result, they enjoy rates between 3.99% and 6.99% for auto loans [2][7].

Some manufacturers offer even better deals - Subaru has advertised rates as low as 1.99% on 60-month terms, while Nissan and Mazda have promoted rates of 2.49% and 2.95%, respectively [7].

Prime (670–719): 5.99% to 9.99%

The prime tier includes credit scores ranging from 670 to 719. While still offering favorable terms, rates for these borrowers are slightly higher than those in the super prime category, typically between 5.99% and 9.99% [2][7]. Factors like the vehicle's age, down payment size, and loan term can influence the exact rate you’re offered.

For example, major Canadian banks such as CIBC, TD, RBC, BMO, Scotiabank, and National Bank start their auto loan rates for prime borrowers at 7.20% [6]. These rates highlight the importance of maintaining a solid credit score to secure better financing options.

Near Prime (620–669): 8.99% to 14.99%

Borrowers in the near prime range, with scores between 620 and 669, face higher interest rates due to moderate risk. Rates typically fall between 8.99% and 14.99% [2][7]. Additionally, lenders may impose stricter conditions, such as limiting the age of the vehicle or requiring a larger down payment.

To put this into perspective, someone with a 720 credit score might pay approximately $435 per month on a $20,000 loan, while a borrower with a 620 score could see monthly payments jump to $565 - a difference of $130 per month [1]. Getting pre-approved can help you understand your borrowing limits and avoid costly long-term loans.

Subprime (Below 620): 10.99% to 29.99%+

Borrowers with credit scores below 620 fall into the subprime category, where rates range from 10.99% to 29.99% [2][7]. For those with scores under 580, rates on used vehicles can climb as high as 34.99%, although the legal maximum in Canada is 35% APR, which includes all fees [2][4][8].

The financial impact of subprime rates is significant. On a $20,000 loan over five years, a borrower in this category might pay over $13,900 in interest, compared to just $4,300 for someone with excellent credit [1]. To offset the higher risk, lenders typically require proof of stable income and employment history. Borrowers in this range may benefit from working with lenders who specialize in credit rebuilding to improve their future financing opportunities.

Other Factors That Affect Your Rate

Your credit score may be a big piece of the puzzle when it comes to your auto loan rate, but it’s not the whole picture. Several other factors can shape the overall cost of your loan and influence your interest rate.

Loan Term Length

The length of your loan term can have a noticeable impact on your interest rate. Shorter terms, like 36 to 48 months, often come with lower rates because they reduce the lender’s risk [7]. On the flip side, longer terms - think 72 to 96 months - tend to carry higher rates. Why? Vehicles lose value quickly, and longer terms increase the chance of owing more than the car is worth (negative equity) [4].

Here’s an example: A $25,000 loan at 7.5% APR over 60 months will cost less in total interest compared to the same loan at 10.9% APR over 84 months - even if the shorter term comes with higher monthly payments [5]. If you’re leaning toward a longer term to keep payments manageable, look for loans that allow early repayment without penalties. This can help you save on interest over time [6].

Vehicle Type and Age

The type and age of the vehicle you’re financing also play a role in determining your rate. New cars generally come with interest rates that are 2–3% lower than those for used cars. That’s because new vehicles are in better condition, have more predictable resale values, and often come with warranties [9].

Used cars, especially older ones, tend to have higher rates. For instance, a 10-year-old car will likely come with a much higher rate than a 2-year-old model [9]. Additionally, many lenders won’t finance vehicles that are more than 10 years old or have over 100,000 miles, so it’s important to check eligibility requirements [7]. If you’re considering a Certified Pre-Owned (CPO) vehicle, you might find a sweet spot. These cars have been inspected thoroughly and sometimes include extended warranties, which can help you qualify for better rates [9].

Down Payment and Income

Your down payment and income level can also influence your interest rate. A larger down payment reduces your loan-to-value (LTV) ratio, which can lower your rate [3][4]. Even a small increase in your down payment might make a noticeable difference [10].

As Rick MacDonnell from GoAuto.ca puts it:

The higher your salary (or, more specifically, the more money you have available after monthly debt payments), the more confidence they will have in you to pay them back on time [3].

Lenders also look at your debt-to-income (DTI) ratio. Stable employment and manageable monthly payments are especially important if you fall into the subprime credit range. For those with less-than-perfect credit, combining a solid down payment with verifiable income can improve your chances of approval and help offset higher interest rates [3][2].

Rate Comparison by Credit Tier

The table below highlights how credit tiers influence loan costs, breaking down key details like interest rates, monthly payments, and total interest for a $20,000 loan over five years:

Credit Tier | Score Range | Typical APR Range | Monthly Payment (for a $20,000 loan, 5 years) | Total Interest Paid |

|---|---|---|---|---|

Super Prime | 760+ | 4.99% – 6.99% | ~$405 | ~$4,300 |

Prime | 700–759 | 6.99% – 9.99% | ~$435 | ~$6,100 |

Near Prime | 640–699 | 9.99% – 15.99% | ~$487 | ~$9,200 |

Subprime | 580–639 | 15.99% – 24.99% | ~$565 | ~$13,900 |

Deep Subprime | Below 580 | 19.99% – 34.99%+ | ~$650–$720 | ~$19,000+ |

Source: Compiled from Canadian market data, 2026 [1][2]

The gap between credit tiers is striking. For a $20,000 loan, Subprime borrowers pay nearly $10,000 more in total interest than those in the Super Prime category. This translates to an extra $160 per month in interest payments alone [1].

When financing larger purchases, the difference becomes even more dramatic. For instance, on a $48,000 vehicle financed over five years, a Super Prime borrower with a 5.39% APR pays around $6,385 in total interest. In contrast, a Deep Subprime borrower with a 14.99% APR faces approximately $19,065 in interest - a staggering $12,680 more [11]. Essentially, Deep Subprime borrowers can end up paying nearly three times the interest of their Super Prime counterparts.

Even a modest credit score improvement of 20–40 points can lead to significant savings, potentially reducing thousands in interest costs [1]. These numbers highlight the financial advantages of improving your credit score, even by a small margin.

What This Means for Borrowers

Your credit score doesn't just influence the interest rate you get - it directly affects how much you'll pay over time. Lenders use your score to gauge risk. A higher score shows you're reliable with payments, which earns you lower interest rates. On the flip side, a lower score signals more risk, leading lenders to charge higher rates to protect themselves [2].

The difference can be staggering. For instance, boosting your credit score from 620 to 700 on a $20,000 loan could save you around $7,800 in interest over five years. That’s a huge reduction in borrowing costs, showing how even modest improvements can translate into substantial savings [1].

Steps to Improve Your Credit Score

The most critical part of your credit score is your payment history. Late payments can have a big impact, so set up automatic payments or reminders to ensure you’re always on time [12]. Another key factor is your credit utilization - try to keep your credit card balances below 30% of your total limit to maintain a strong score [19,11].

Be cautious about applying for new credit cards or loans before securing auto financing. Too many hard inquiries in a short period can temporarily lower your score [12]. Also, keep older credit accounts open if possible. Closing them can reduce the average age of your accounts, which might hurt your score. And don’t forget: negative marks like late payments can stick to your credit report for up to six years in Canada [12].

Finding Lenders That Work With All Credit Types

Improving your credit score is important, but finding the right lender can make a big difference too. Traditional banks often have the lowest rates, but they usually require excellent credit to qualify. If your credit is less than perfect, there are specialized lenders that focus more on your income stability and overall financial situation than just your credit score [5,20]. These lenders might consider factors like your employment history and steady income to approve loans that conventional banks might reject.

For example, Hello Motors (https://hellomotors.ca) helps borrowers with all types of credit histories secure flexible auto financing. They take a holistic view of your financial situation to offer tailored options that fit your budget. Look for lenders that provide "open" loans, which let you pay off your loan early without penalties. This is especially helpful if you plan to refinance later, a common strategy among Canadian borrowers who improve their credit with 12 to 18 months of on-time payments [2,5].